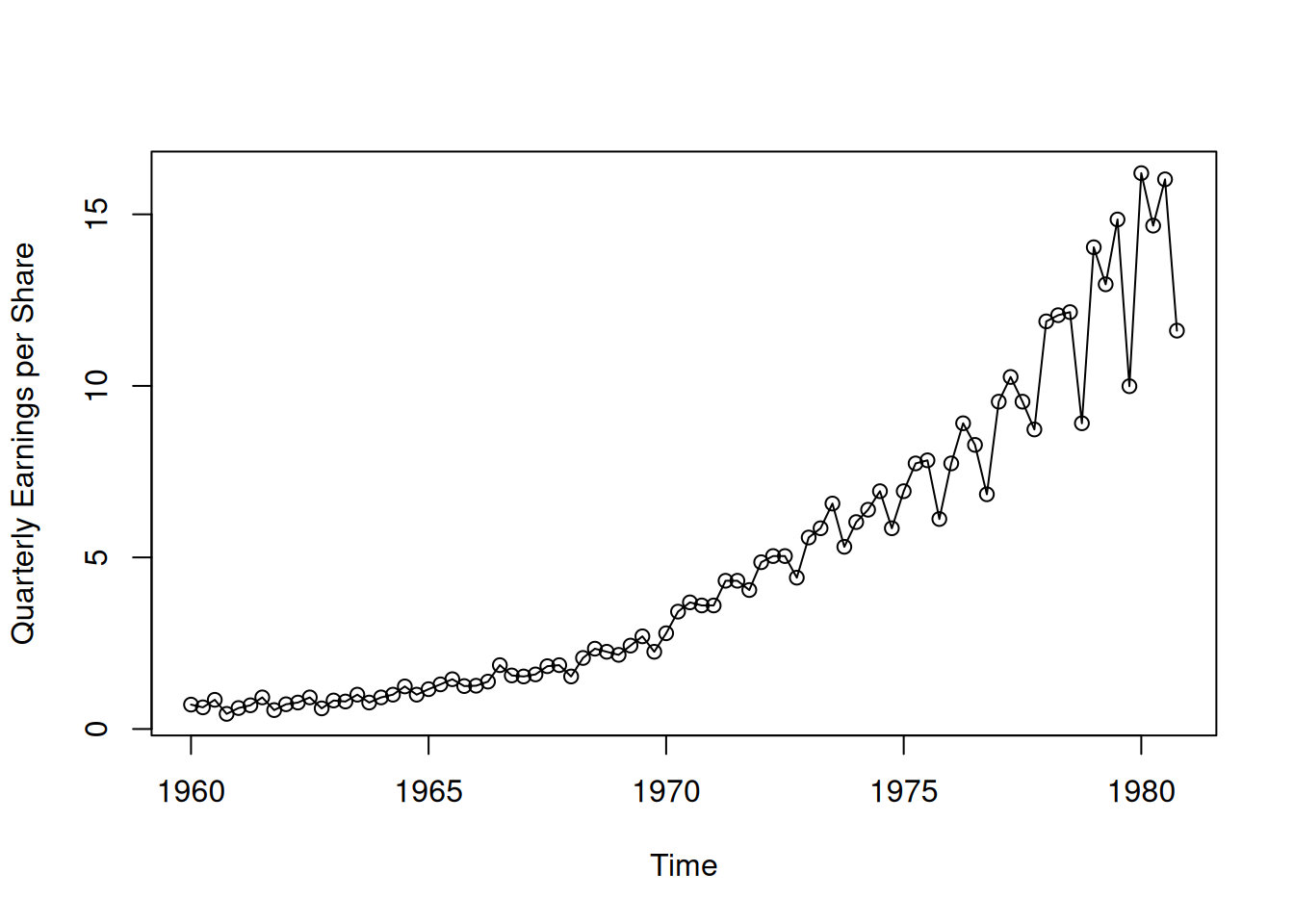

library(astsa) # datos jj, globtemp

plot(jj, type = "o", ylab = "Quarterly Earnings per Share")

El objetivo es ilustrar, con series de tiempo reales, los patrones típicos y las preguntas estadísticas frecuentes que interesan a un analista. Varios casos:

Datos: \(n=84\) trimestres (21 años), de Q1-1960 a Q4-1980.

Patrones: tendencia creciente y estacionalidad trimestral marcada.

Enfoque típico: modelar \(y_t\) como

\[ y_t = \text{tendencia}_t + \text{estacionalidad}_{q(t)} + \varepsilon_t, \]

con \(q(t)\in\{1,2,3,4\}\), y evaluar su estructura (capítulos posteriores).

library(astsa) # datos jj, globtemp

plot(jj, type = "o", ylab = "Quarterly Earnings per Share")

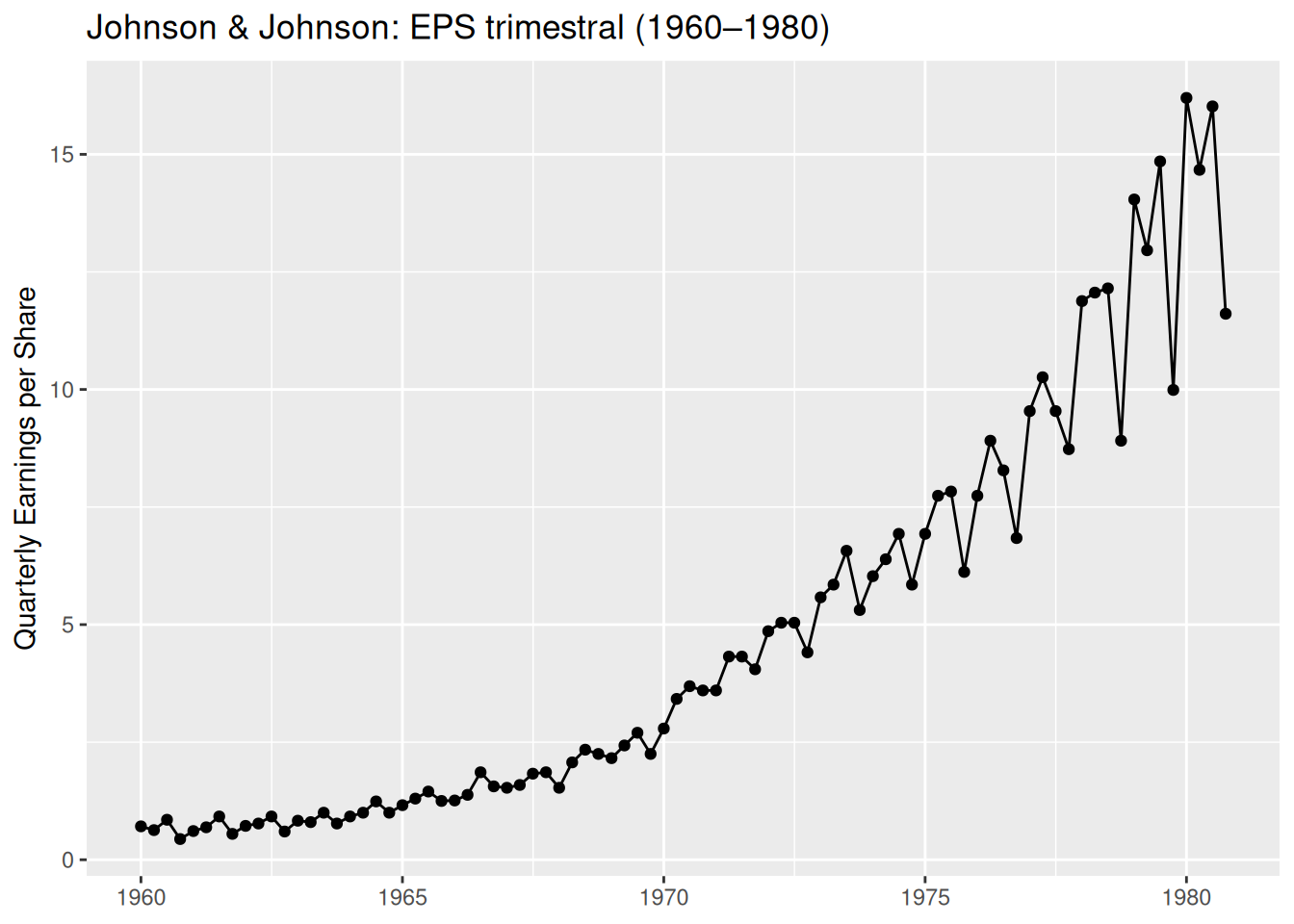

O usando tidyverse:

# Paquetes

library(tidyverse)── Attaching core tidyverse packages ──────────────────────── tidyverse 2.0.0 ──

✔ dplyr 1.1.4 ✔ readr 2.1.5

✔ forcats 1.0.0 ✔ stringr 1.5.2

✔ ggplot2 4.0.0 ✔ tibble 3.3.0

✔ lubridate 1.9.4 ✔ tidyr 1.3.1

✔ purrr 1.1.0

── Conflicts ────────────────────────────────────────── tidyverse_conflicts() ──

✖ dplyr::filter() masks stats::filter()

✖ dplyr::lag() masks stats::lag()

ℹ Use the conflicted package (<http://conflicted.r-lib.org/>) to force all conflicts to become errorslibrary(zoo) # as.yearqtr

Attaching package: 'zoo'

The following objects are masked from 'package:base':

as.Date, as.Date.numericlibrary(lubridate) # manejo de fechas

library(astsa)

# Convertir ts -> tibble con fecha trimestral

jj_tbl <- tibble(

date = as.Date(as.yearqtr(time(jj))), # Q1..Q4 a fecha (fin de trimestre)

eps = as.numeric(jj)

)

# Gráfico

jj_tbl %>%

ggplot(aes(date, eps)) +

geom_line() +

geom_point() +

labs(

title = "Johnson & Johnson: EPS trimestral (1960–1980)",

x = NULL, y = "Quarterly Earnings per Share"

)

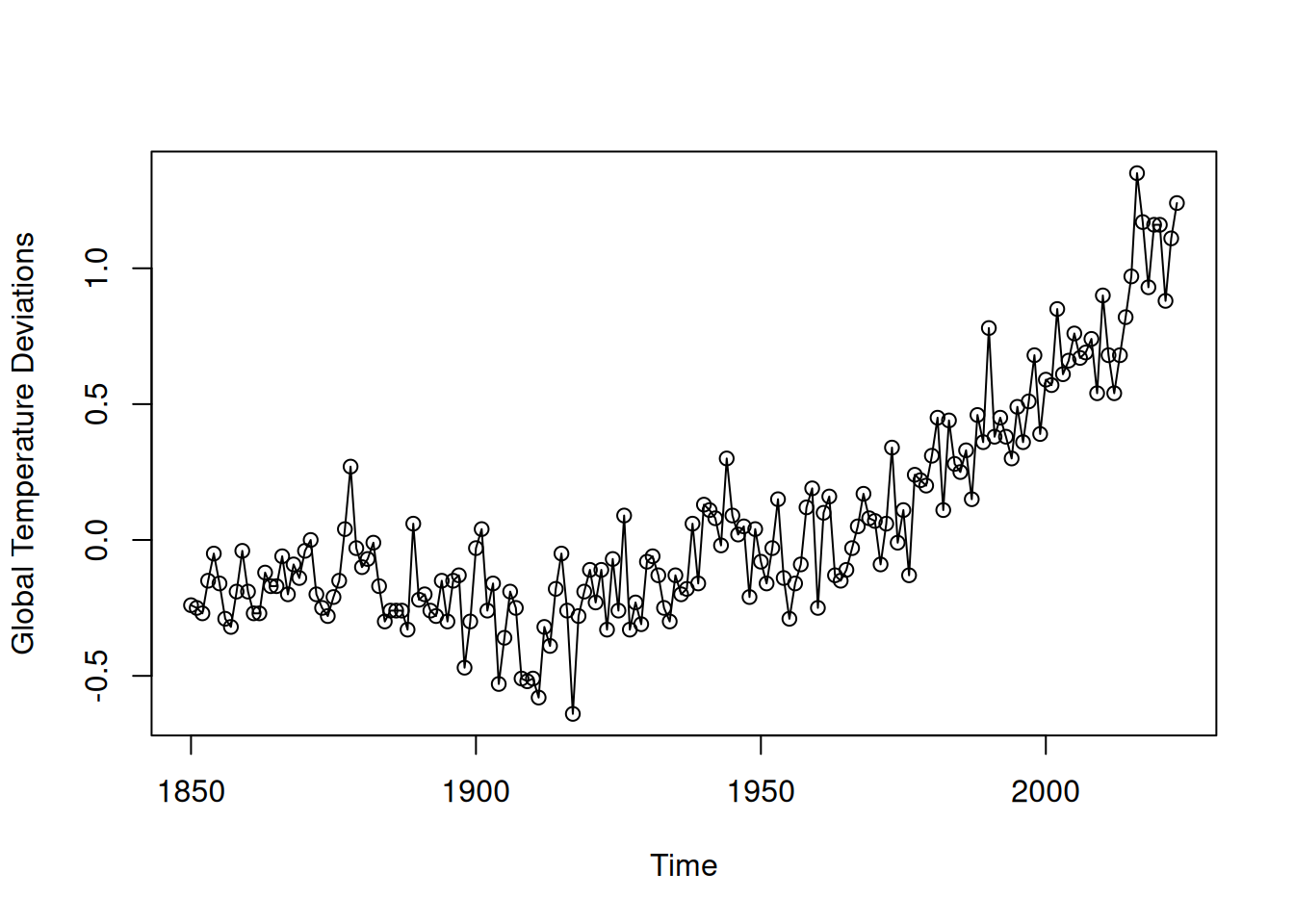

Datos: índice de temperatura media global tierra-océano (base 1951–1980, Hansen et al. [89] actualizado).

Variable: desviaciones en °C respecto a la media 1951–1980:

\[ T'_t = T_t - \bar{T}_{1951-1980} \]

Patrones observados:

Pregunta clave: ¿tendencia causada por procesos naturales o antropogénicos?

Observación: cambios porcentuales similares han ocurrido en escalas de 100 años (véase problema 2.8 con 634 años de sedimentos glaciares).

Interés principal: tendencia a largo plazo, no periodicidades.

Código R original (base R)

library(astsa)

plot(gtemp_both, type = "o", ylab = "Global Temperature Deviations")

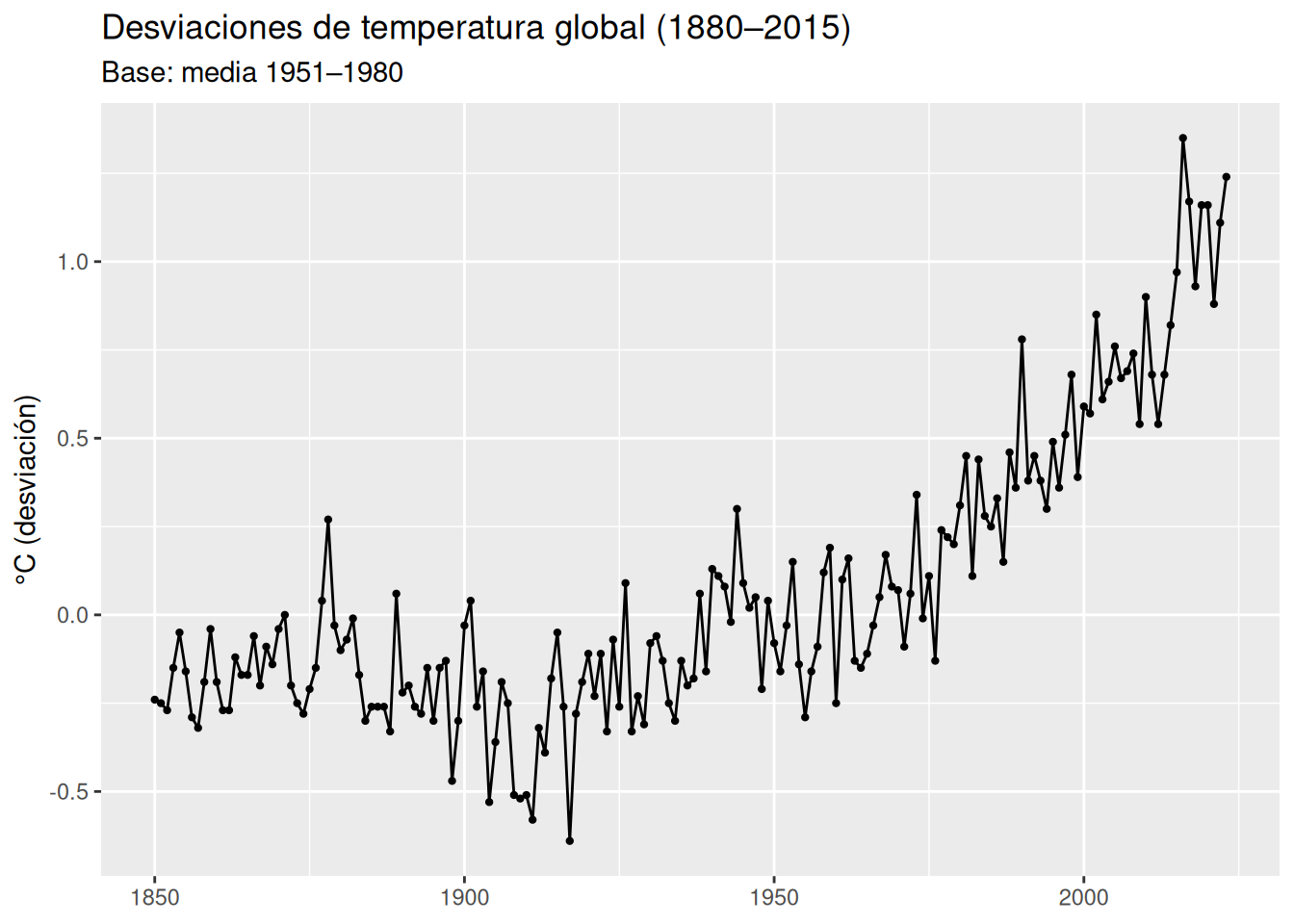

Usando tidyverse:

library(tidyverse)

library(astsa)

# Convertir ts -> tibble con año y desviación

gt_tbl <- tibble(

year = as.integer(floor(time(gtemp_both))),

temp_devC = as.numeric(gtemp_both)

)

# Gráfico con ggplot2

gt_tbl %>%

ggplot(aes(year, temp_devC)) +

geom_line() +

geom_point(size = 0.8) +

labs(

title = "Desviaciones de temperatura global (1880–2015)",

subtitle = "Base: media 1951–1980",

x = NULL, y = "°C (desviación)"

)

En términos generales, el análisis puede comenzar con un modelo aditivo simple:

\[ T'_t = \mu_t + \varepsilon_t \]

donde:

El objetivo inicial es estimar \(\mu_t\) y evaluar si el patrón observado es estadísticamente significativo y consistente con hipótesis de cambio climático.

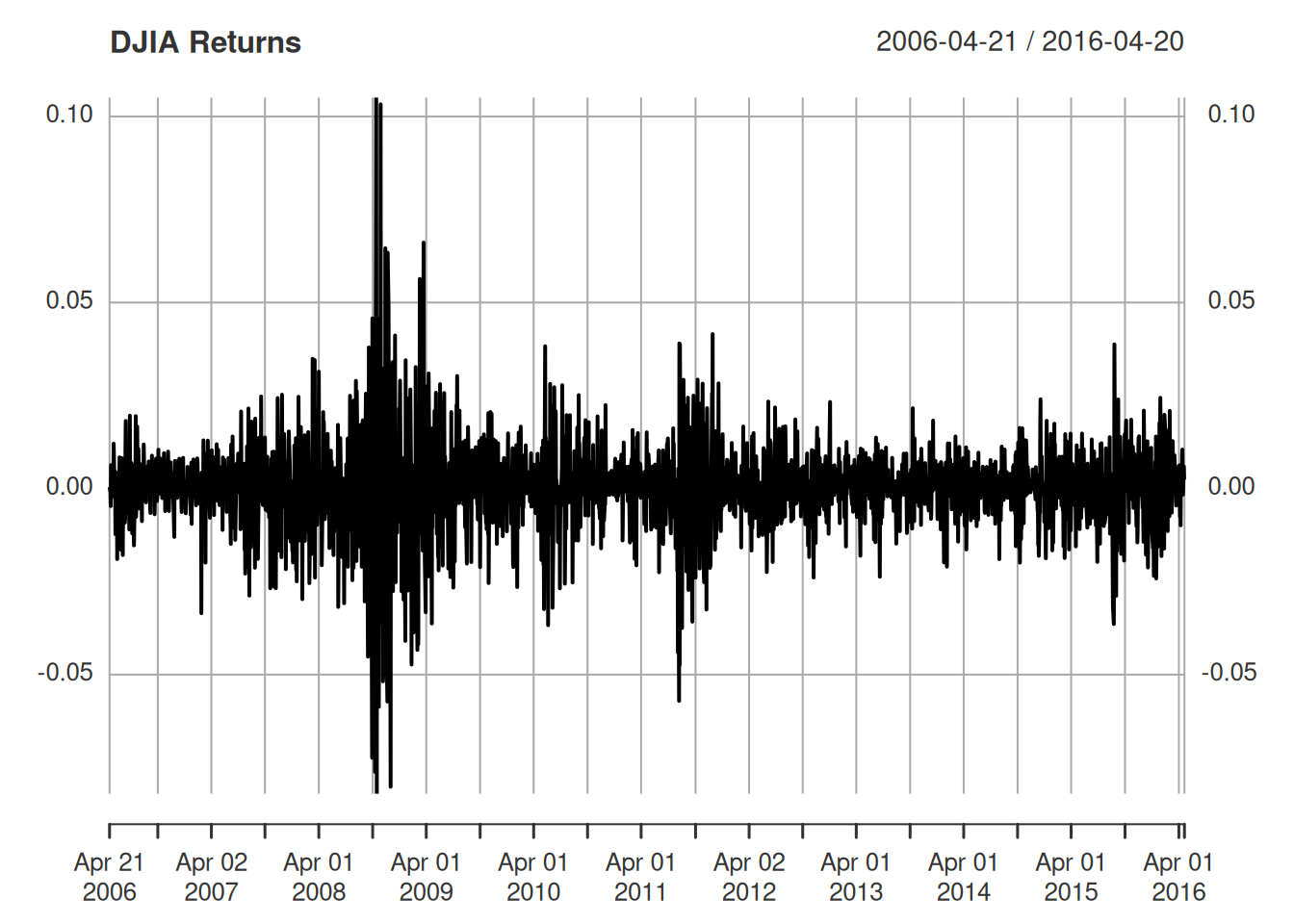

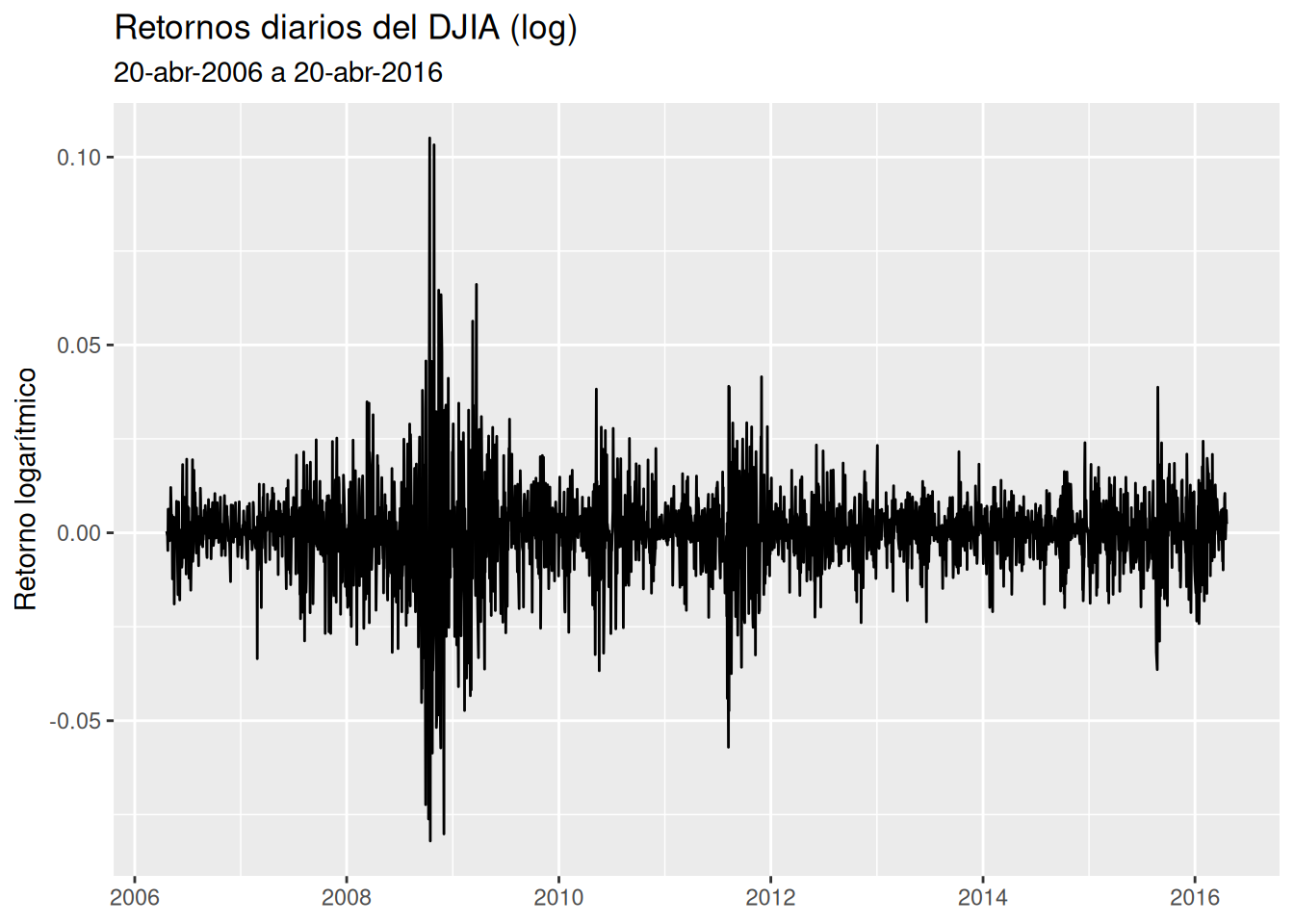

Datos: retornos diarios del DJIA del 20-abr-2006 al 20-abr-2016.

Fórmula del retorno:

\[ r_t = \frac{x_t - x_{t-1}}{x_{t-1}}, \quad 1+r_t = \frac{x_t}{x_{t-1}}, \]

y en forma logarítmica:

\[ \log(1+r_t) = \log(x_t) - \log(x_{t-1}) \approx r_t. \]

Características:

Problema típico: pronóstico de volatilidad.

Modelos relevantes: ARCH, GARCH (Engle, Bollerslev) y volatilidad estocástica (Harvey, Ruiz, Shephard).

Datos disponibles en astsa; para procesamiento se requiere xts.

Código R original (base R)

library(xts)

######################### Warning from 'xts' package ##########################

# #

# The dplyr lag() function breaks how base R's lag() function is supposed to #

# work, which breaks lag(my_xts). Calls to lag(my_xts) that you type or #

# source() into this session won't work correctly. #

# #

# Use stats::lag() to make sure you're not using dplyr::lag(), or you can add #

# conflictRules('dplyr', exclude = 'lag') to your .Rprofile to stop #

# dplyr from breaking base R's lag() function. #

# #

# Code in packages is not affected. It's protected by R's namespace mechanism #

# Set `options(xts.warn_dplyr_breaks_lag = FALSE)` to suppress this warning. #

# #

###############################################################################

Attaching package: 'xts'The following objects are masked from 'package:dplyr':

first, lastdjiar = diff(log(djia$Close))[-1] # retornos aproximados

plot(djiar, main = "DJIA Returns", type = "l")

Código R en tidyverse

library(tidyverse)

library(astsa) # datos djia

library(lubridate)

# Convertir a tibble con retornos logarítmicos

djia_tbl <- as_tibble(djia) %>%

mutate(date = as.Date(index(djia))) %>%

arrange(date) %>%

mutate(

log_ret = log(Close) - lag(log(Close))

) %>%

filter(!is.na(log_ret))

# Gráfico de retornos

djia_tbl %>%

ggplot(aes(date, log_ret)) +

geom_line() +

labs(

title = "Retornos diarios del DJIA (log)",

subtitle = "20-abr-2006 a 20-abr-2016",

x = NULL, y = "Retorno logarítmico"

)

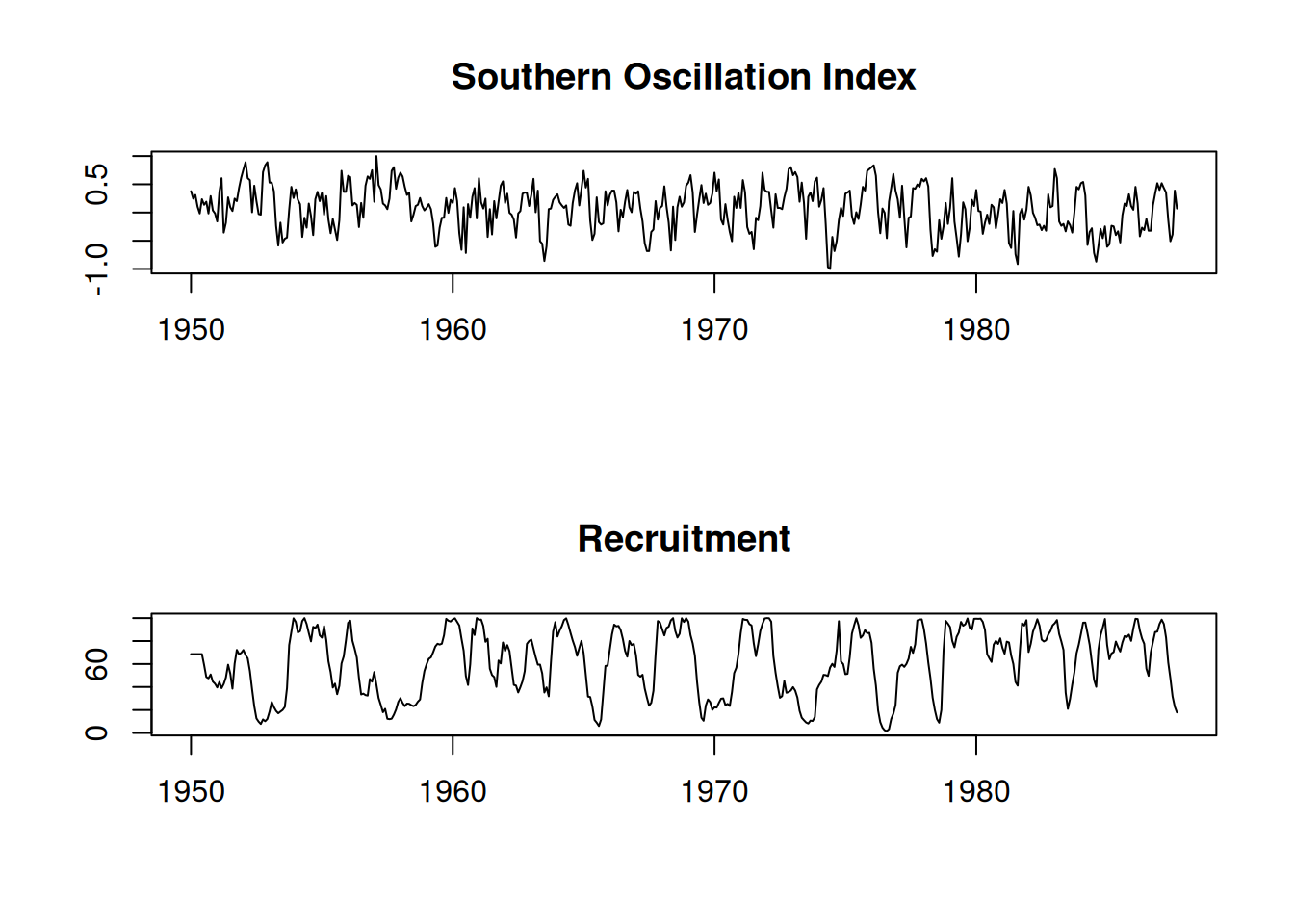

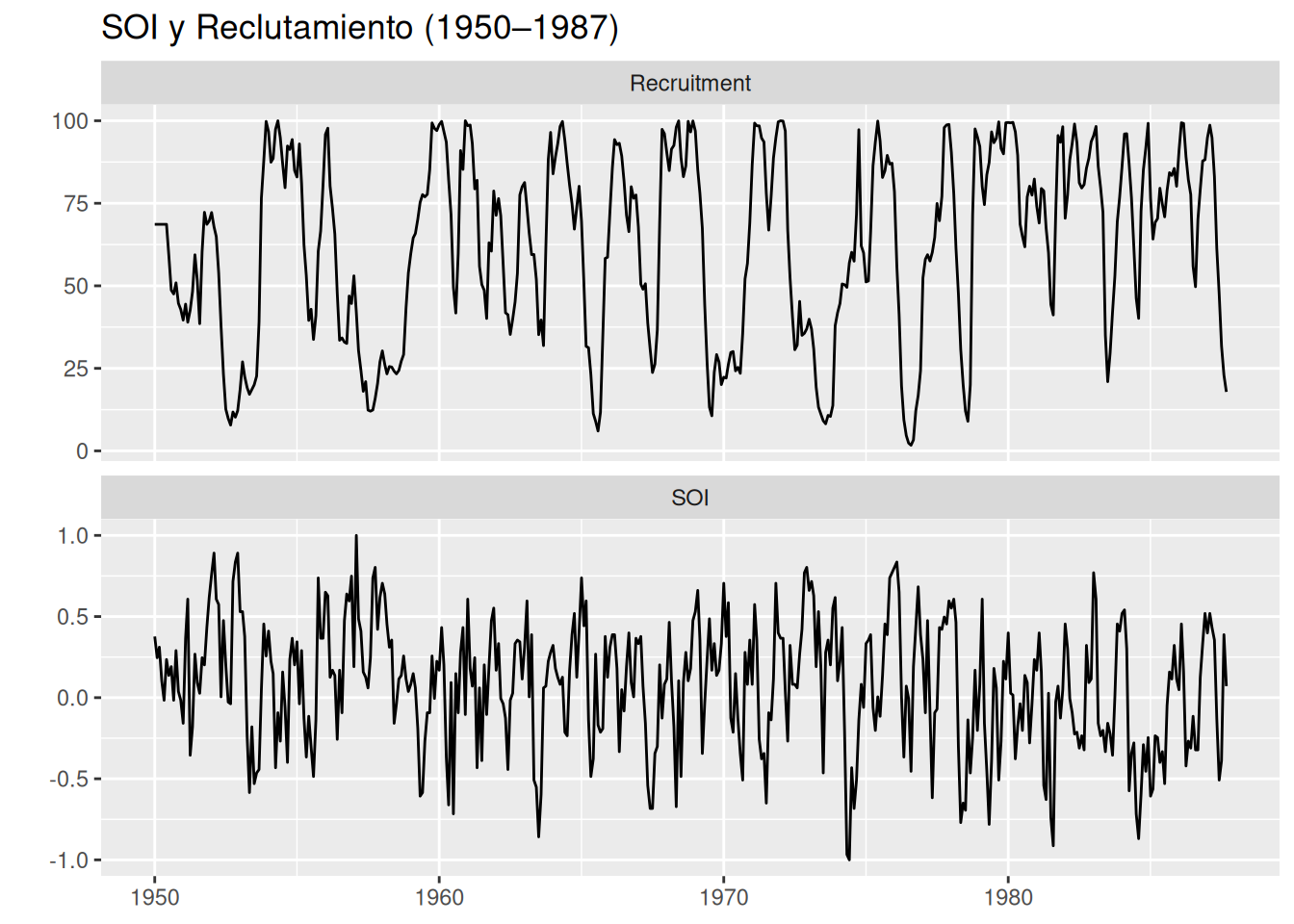

Datos mensuales:

Fenómenos:

El Niño: calentamiento cada 3–7 años en el Pacífico central.

Ciclos detectados:

Interés:

Identificar frecuencias dominantes en las series.

Analizar relación SOI–reclutamiento:

\[ \text{Recruitment}_t \; \text{vs} \; \text{SOI}_t \]

mediante regresión o modelos de función de transferencia.

Motivación: La temperatura oceánica puede influir en la dinámica de la población de peces.

Código R original (base R)

par(mfrow = c(2,1))

plot(soi, ylab = "", xlab = "", main = "Southern Oscillation Index")

plot(rec, ylab = "", xlab = "", main = "Recruitment")

Código R en tidyverse

library(tidyverse)

library(astsa) # datos soi y rec

# Conversión de ts a tibble

soi_tbl <- tibble(

date = as.Date(time(soi)),

SOI = as.numeric(soi)

)

rec_tbl <- tibble(

date = as.Date(time(rec)),

Recruitment = as.numeric(rec)

)

# Graficar ambas series en paneles separados

bind_rows(

soi_tbl %>% mutate(series = "SOI", value = SOI) %>% select(date, series, value),

rec_tbl %>% mutate(series = "Recruitment", value = Recruitment) %>% select(date, series, value)

) %>%

ggplot(aes(date, value)) +

geom_line() +

facet_wrap(~series, ncol = 1, scales = "free_y") +

labs(

title = "SOI y Reclutamiento (1950–1987)",

x = NULL, y = ""

)

Una serie de tiempo se modela como un conjunto de variables aleatorias ordenadas temporalmente:

\[ x_1, x_2, x_3, \dots \]

Conjunto genérico: \(\{x_t\}\), donde \(t\) es discreto (\(t = 0, \pm 1, \pm 2, \dots\)).

Realización: valores observados de un proceso estocástico.

Notación: se usa “serie de tiempo” para el proceso y su realización.

Representación gráfica:

Suavidad:

Diferencias en suavidad provienen de correlación serial:

\[ x_t \text{ depende de } x_{t-1}, x_{t-2}, \dots \]

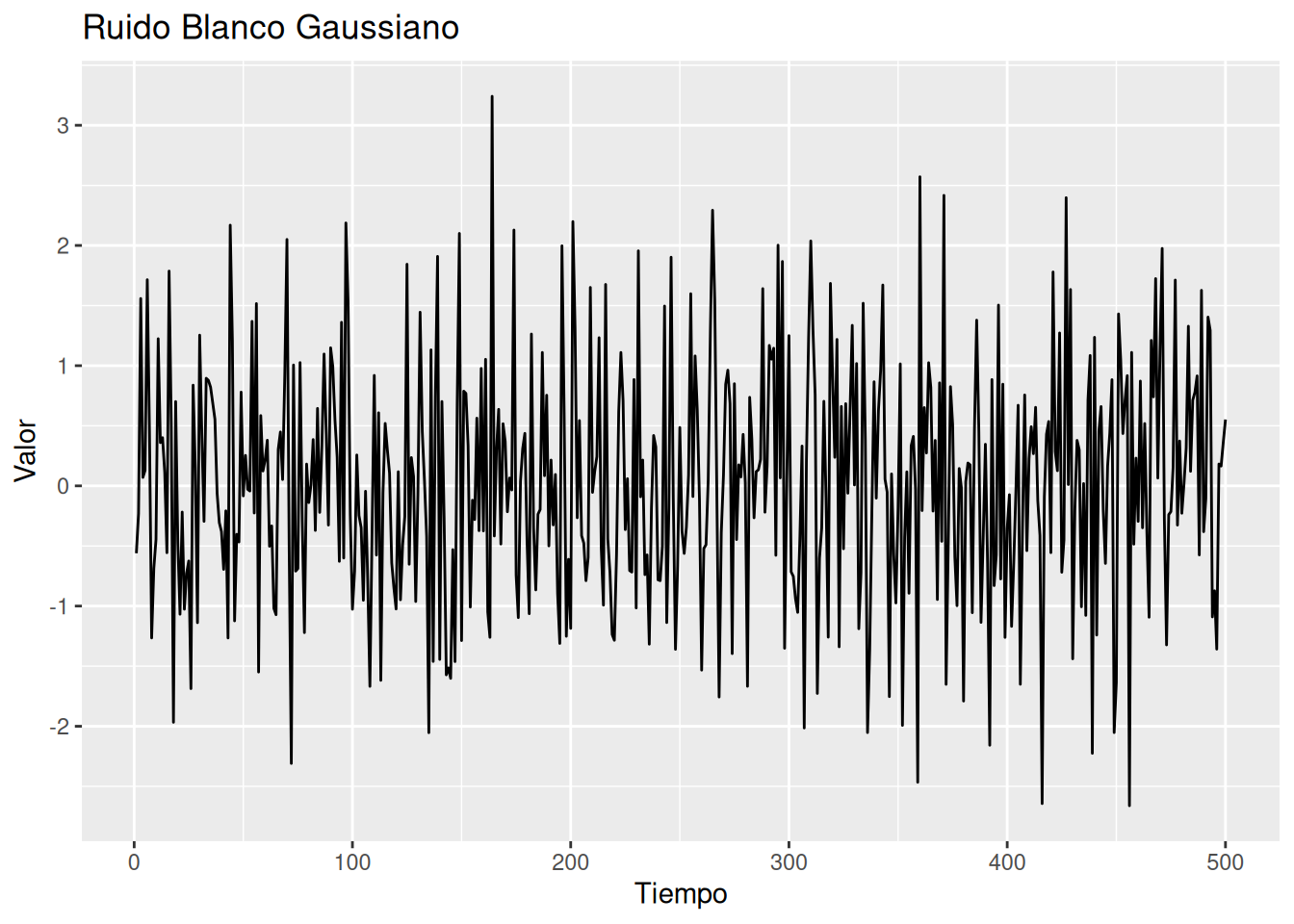

set.seed(123)

w <- rnorm(500, 0, 1) %>% ts()

# Convertir a tibble para ggplot

w_df <- tibble(

tiempo = seq_along(w),

valor = as.numeric(w)

)

ggplot(w_df, aes(x = tiempo, y = valor)) +

geom_line() +

labs(title = "Ruido Blanco Gaussiano", x = "Tiempo", y = "Valor")

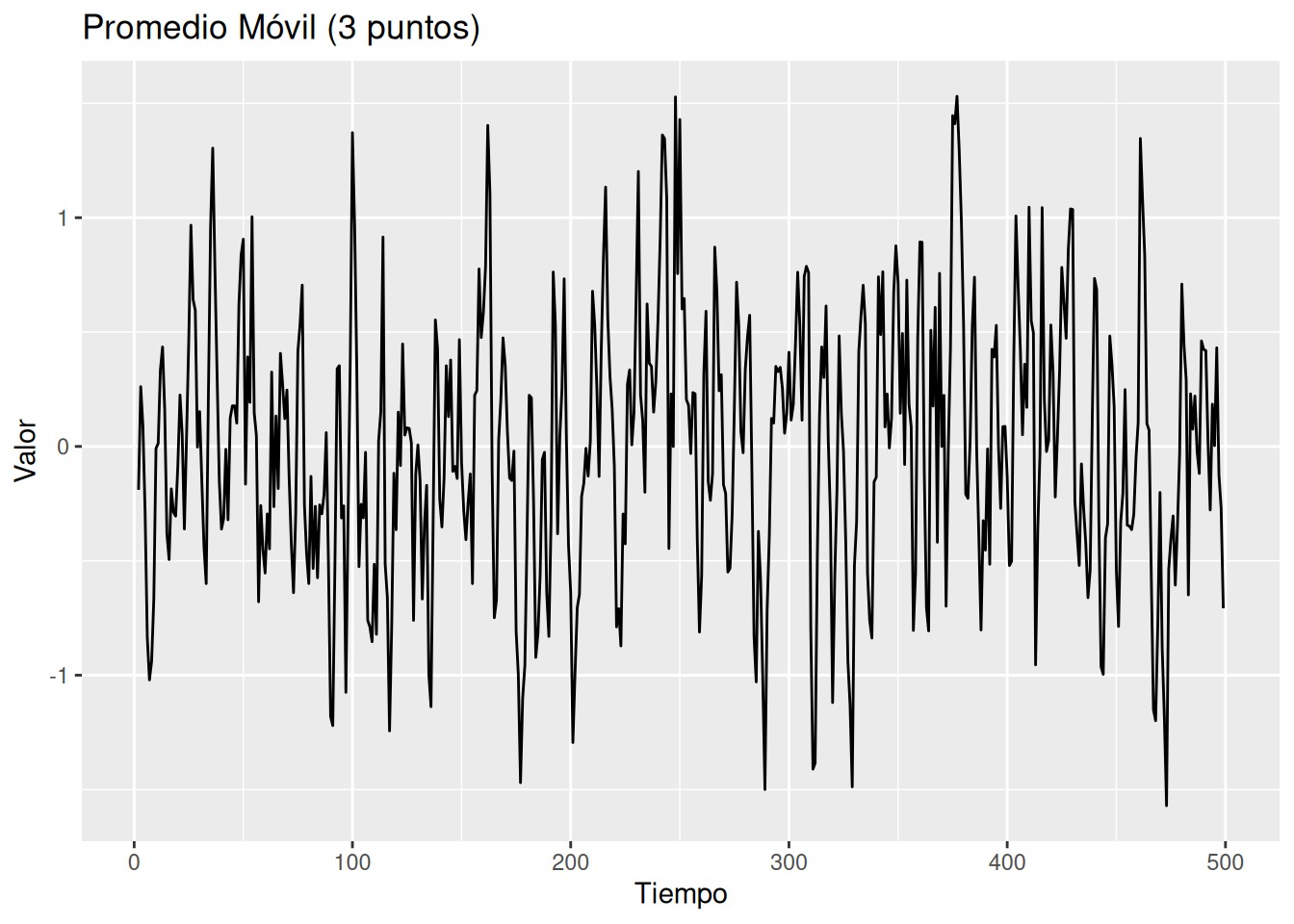

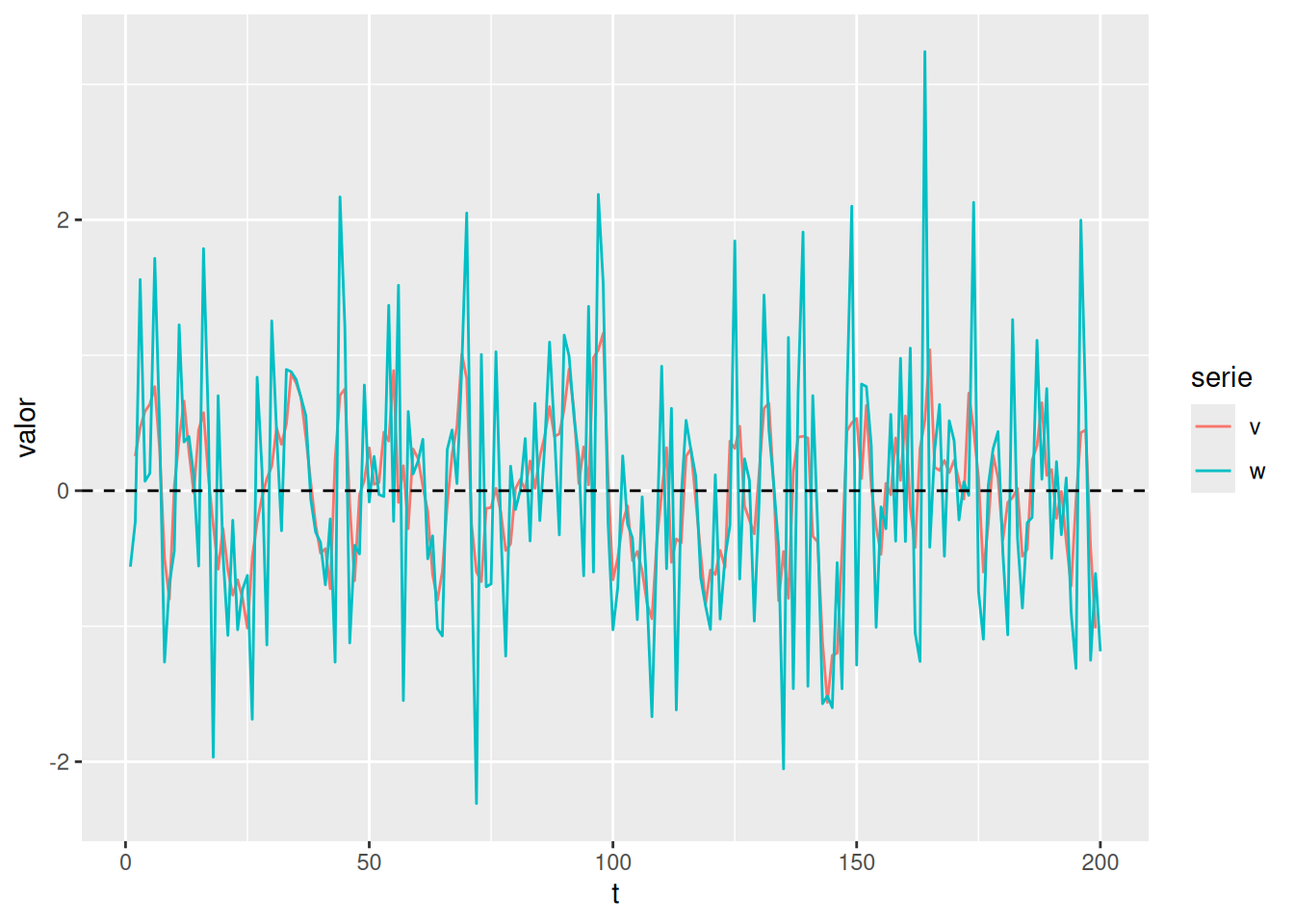

Promedio móvil simétrico:

\[ v_t = \frac{1}{3}(w_{t-1} + w_t + w_{t+1}) \]

Suaviza la serie, elimina oscilaciones rápidas.

w <- rnorm(500, 0, 1)

v <- stats::filter(w, sides = 2, filter = rep(1/3, 3))

# Convertir a tibble para graficar

v_df <- tibble(

tiempo = seq_along(v),

valor = as.numeric(v)

)

ggplot(v_df, aes(x = tiempo, y = valor)) +

geom_line() +

labs(title = "Promedio Móvil (3 puntos)", x = "Tiempo", y = "Valor")Warning: Removed 2 rows containing missing values or values outside the scale range

(`geom_line()`).

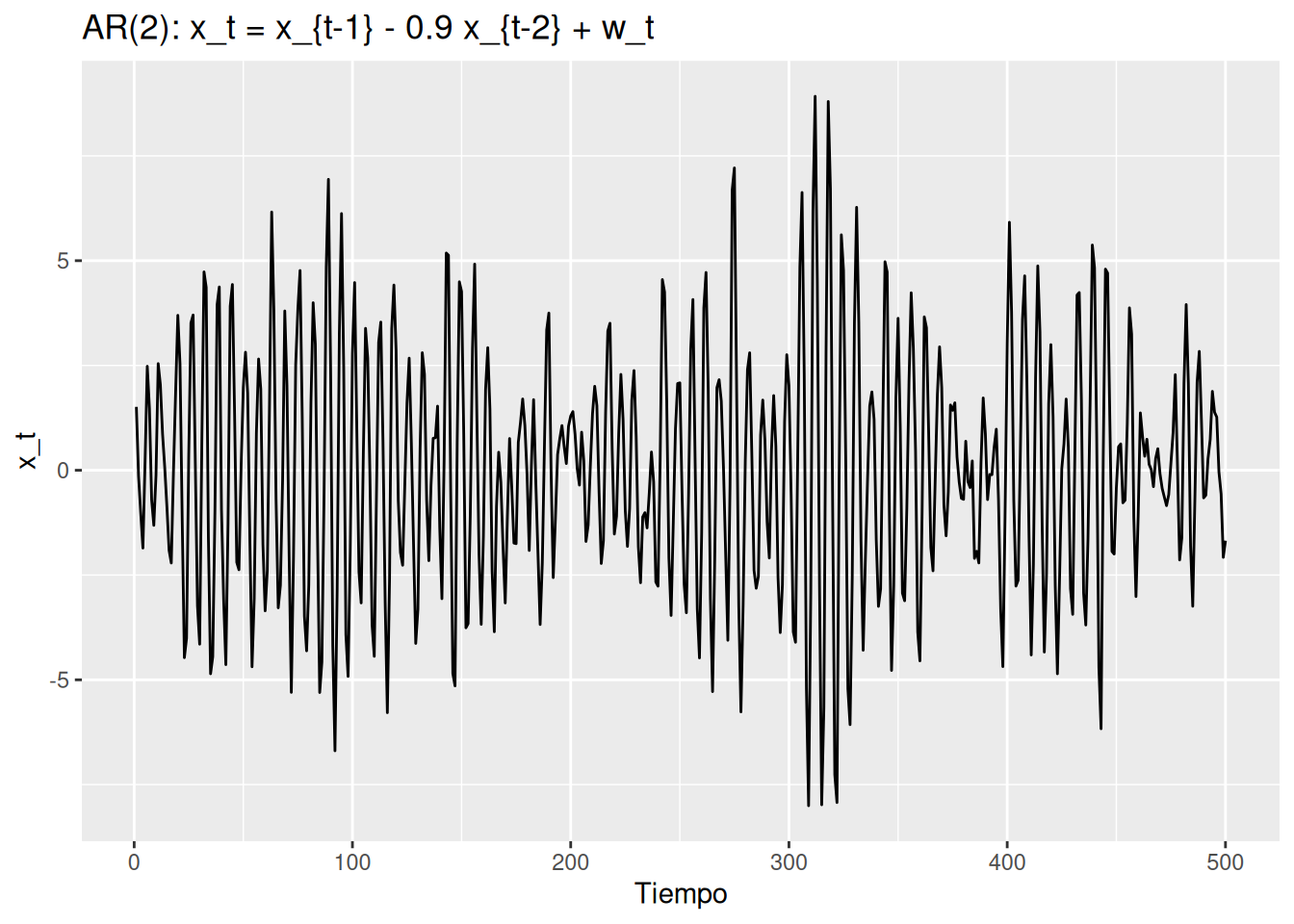

Modelo AR(2):

\[ x_t = x_{t-1} - 0.9 x_{t-2} + w_t \]

Genera comportamiento periódico.

w_ext <- rnorm(550, 0, 1) # extra para “calentar” el filtro

x <- stats::filter(w_ext, filter = c(1, -0.9), method = "recursive")[-(1:50)]

ar_df <- tibble(

tiempo = 1:500,

x = as.numeric(x)

)

ggplot(ar_df, aes(tiempo, x)) +

geom_line() +

labs(title = "AR(2): x_t = x_{t-1} - 0.9 x_{t-2} + w_t", x = "Tiempo", y = "x_t")

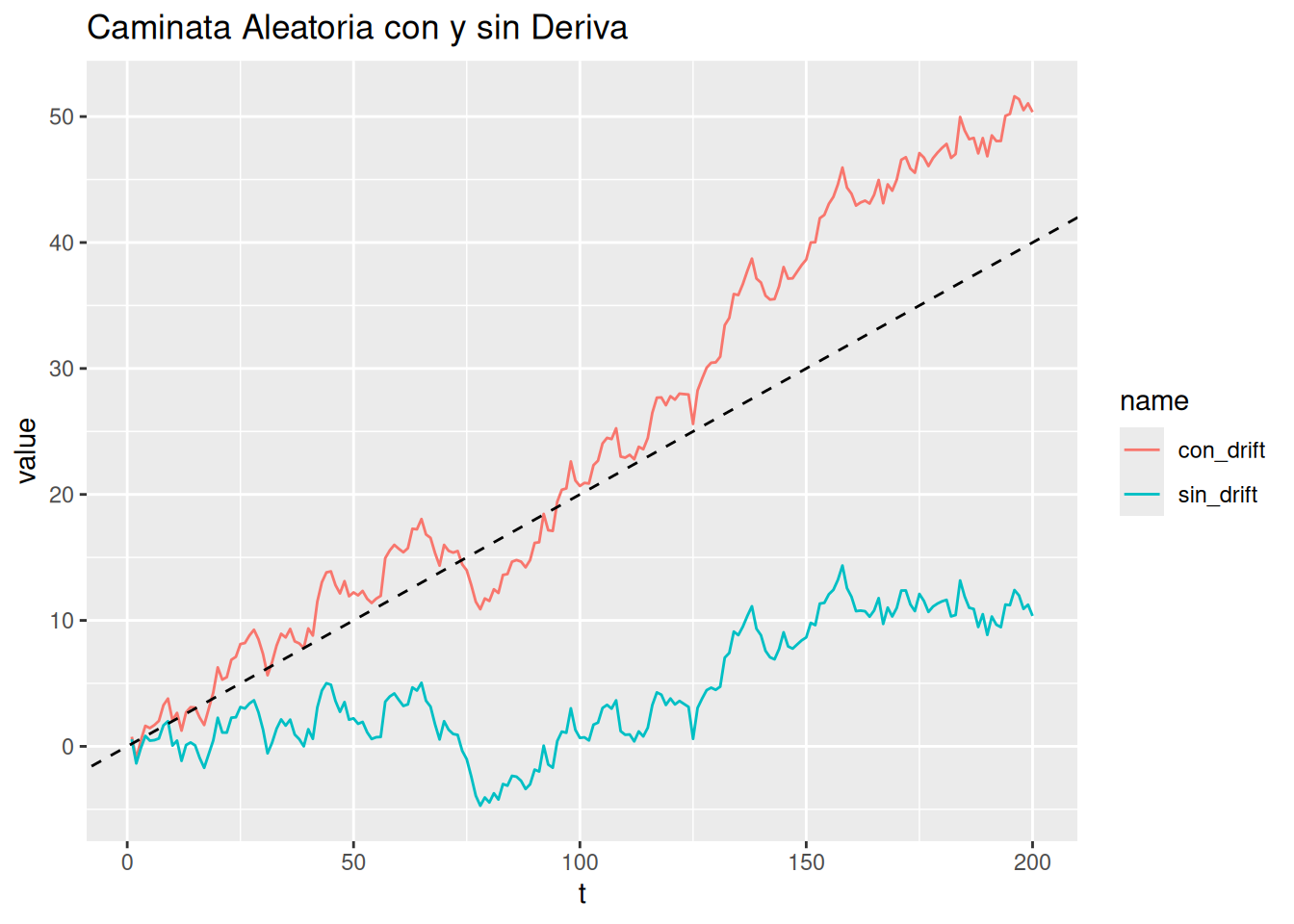

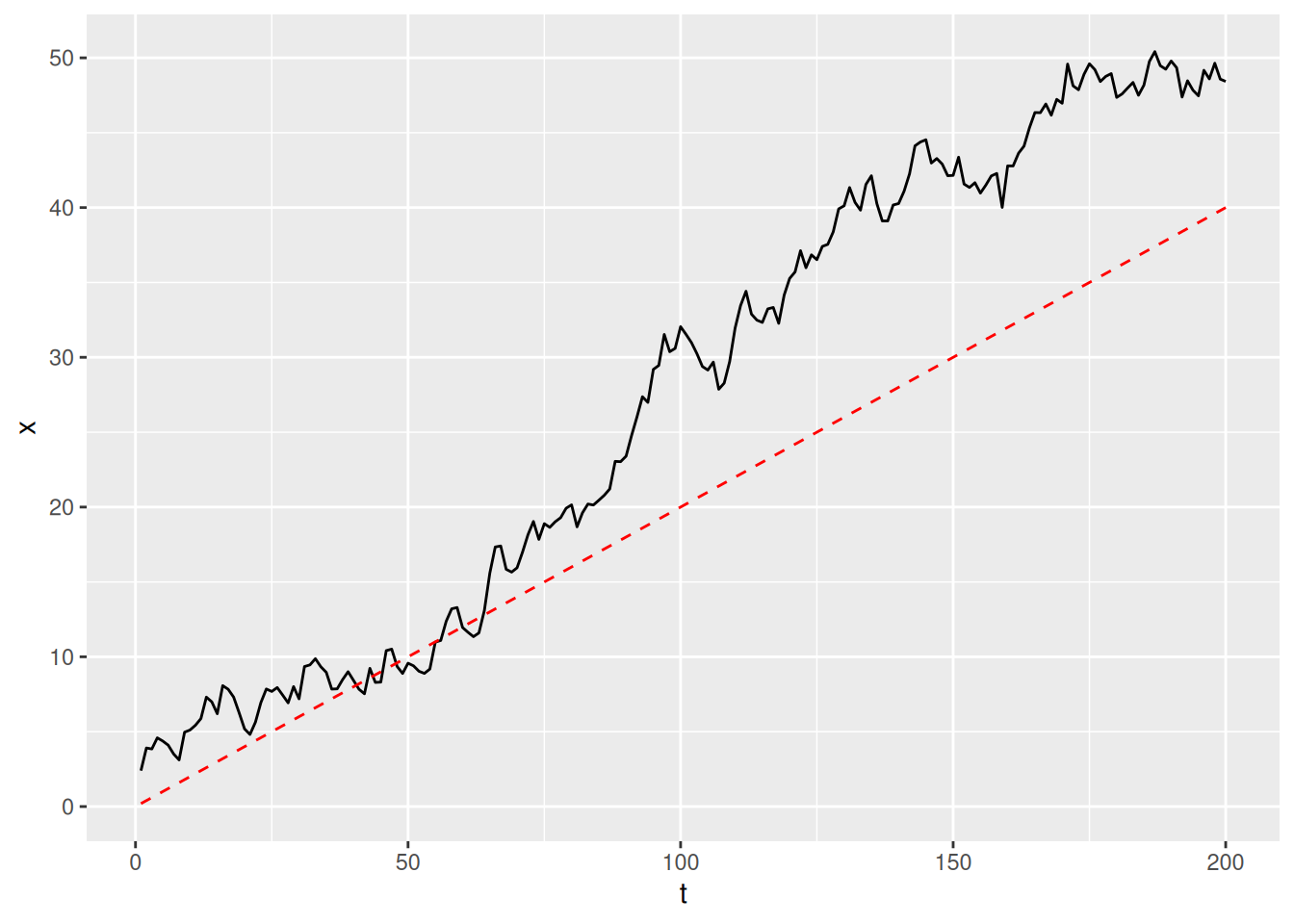

Modelo:

\[ x_t = \delta + x_{t-1} + w_t \]

Forma acumulada:

\[ x_t = \delta t + \sum_{j=1}^t w_j \]

set.seed(154)

w <- rnorm(200)

x <- cumsum(w)

xd <- cumsum(w + 0.2)

tibble(t = 1:200, sin_drift = x, con_drift = xd) %>%

pivot_longer(-t) %>%

ggplot(aes(t, value, color = name)) +

geom_line() +

geom_abline(intercept = 0, slope = 0.2, linetype = "dashed") +

labs(title = "Caminata Aleatoria con y sin Deriva")

Modelo:

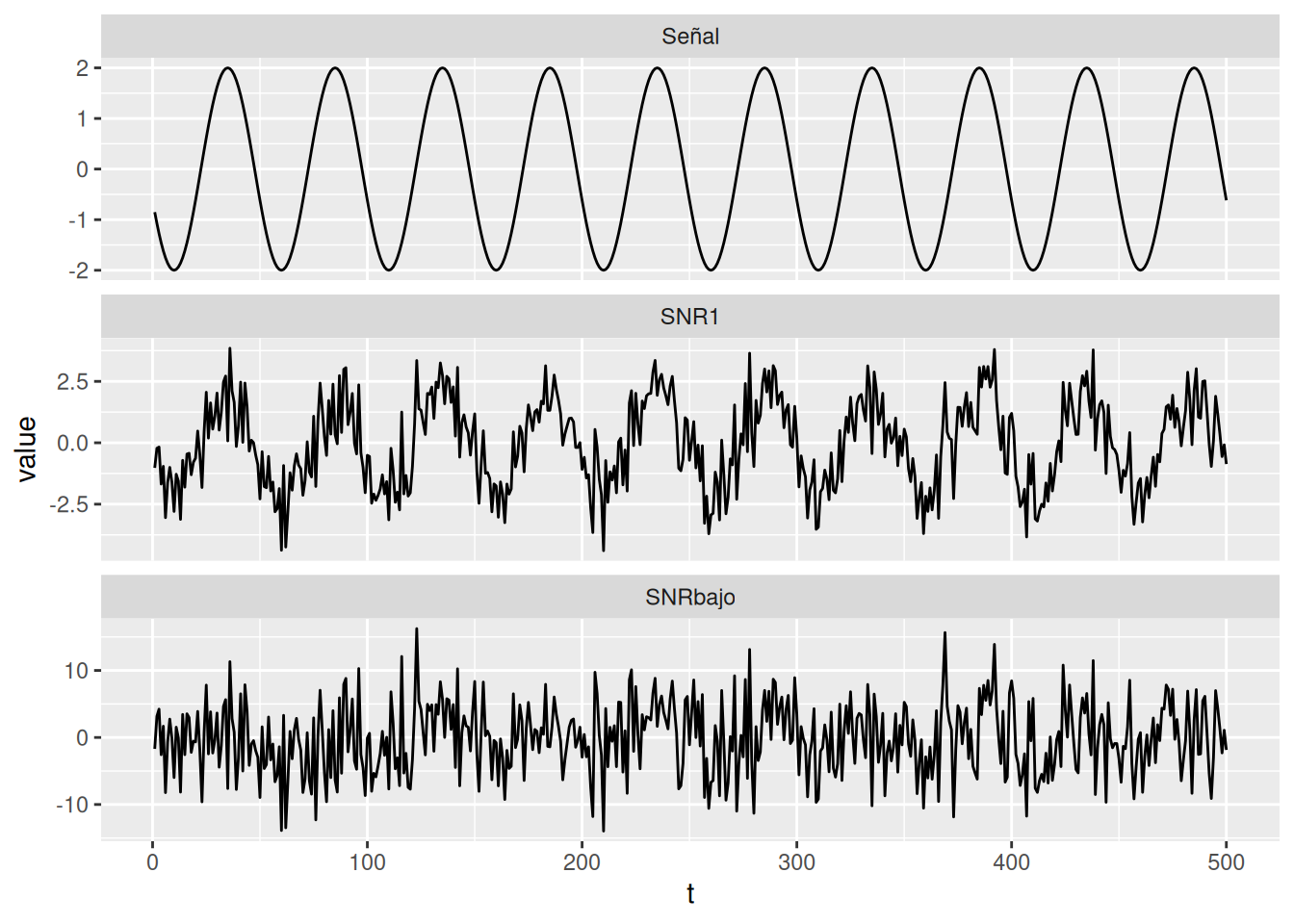

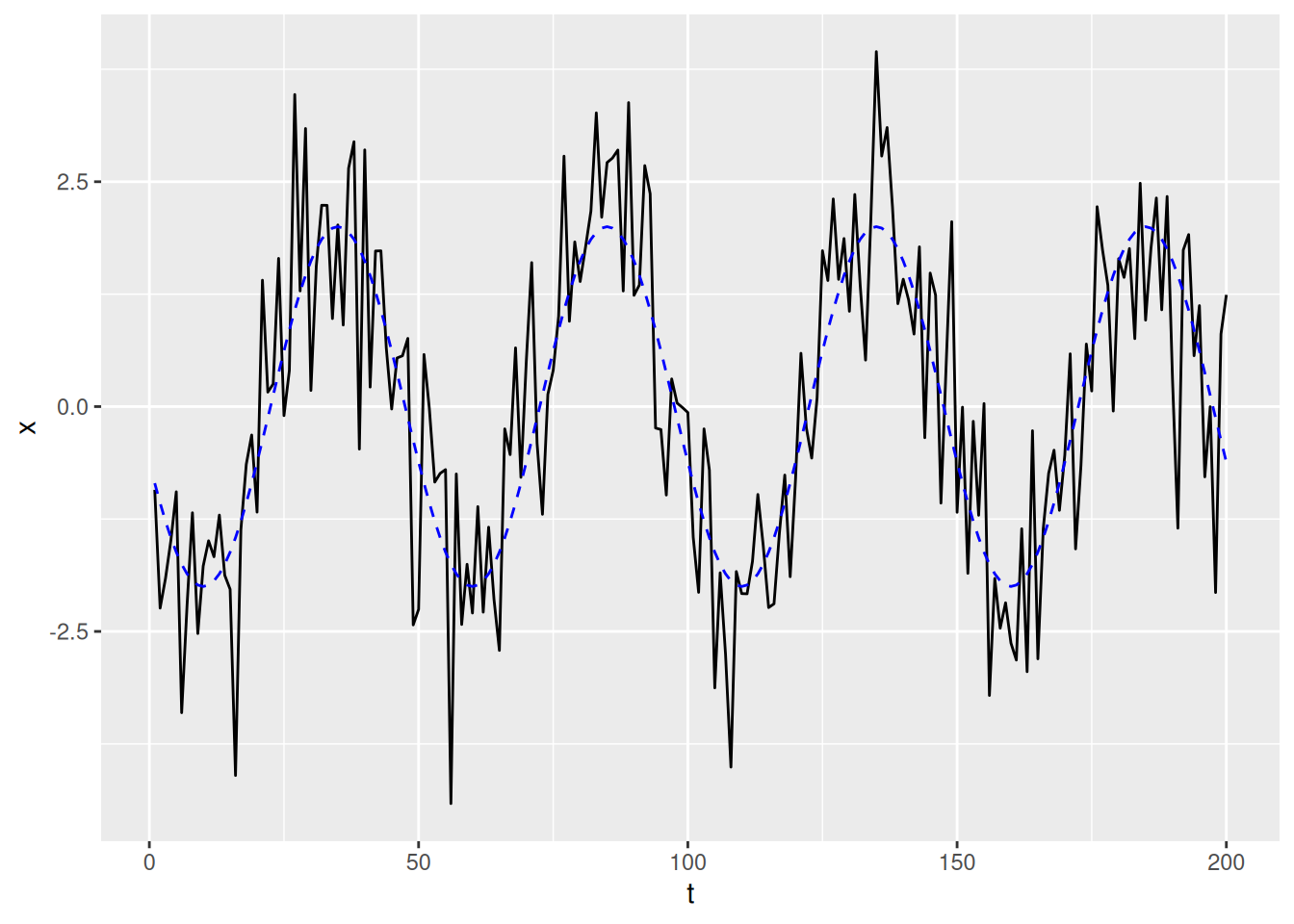

\[ x_t = 2 \cos\left( 2\pi \frac{t + 15}{50} \right) + w_t \]

Forma general:

\[ A\cos(2\pi \omega t + \phi) \]

donde \(A = 2\), \(\omega = 1/50\), \(\phi = 0.6\pi\).

Relación señal/ruido (SNR): mayor SNR → señal más detectable.

t <- 1:500

signal <- 2 * cos(2 * pi * t / 50 + 0.6 * pi)

w <- rnorm(500, 0, 1)

tibble(

t,

Señal = signal,

SNR1 = signal + w,

SNRbajo = signal + 5 * w

) %>%

pivot_longer(-t) %>%

ggplot(aes(t, value)) +

geom_line() +

facet_wrap(~name, scales = "free_y", ncol = 1)

Forma:

\[ x_t = s_t + v_t \]

Aplicaciones: detección de señales, estimación de tendencias, componentes estacionales.

\[ F_{t_1, t_2, \ldots, t_n}(c_1, c_2, \ldots, c_n) = \Pr(x_{t_1} \leq c_1, \, x_{t_2} \leq c_2, \ldots, x_{t_n} \leq c_n) \]

Prácticamente difícil de trabajar salvo en el caso gaussiano.

Usualmente se analizan las marginales:

Definición:

\[ \mu_t = E(x_t) = \int_{-\infty}^\infty x f_t(x) dx \]

set.seed(123)

n <- 200

w <- rnorm(n)

v <- stats::filter(w, rep(1/3, 3), sides = 2)

tibble(t = 1:n, w = w, v = as.numeric(v)) %>%

pivot_longer(-t, names_to = "serie", values_to = "valor") %>%

ggplot(aes(t, valor, color = serie)) +

geom_line() +

geom_hline(yintercept = 0, linetype = "dashed")Warning: Removed 2 rows containing missing values or values outside the scale range

(`geom_line()`).

\[ x_t = \delta t + \sum_{j=1}^t w_j \]

delta <- 0.2

x <- cumsum(rnorm(n)) + delta*(1:n)

tibble(t = 1:n, x = x, mean_f = delta*(1:n)) %>%

ggplot(aes(t, x)) +

geom_line() +

geom_line(aes(y = mean_f), color = "red", linetype = "dashed")

\[ x_t = 2 \cos\!\left(2\pi \tfrac{t+15}{50}\right) + w_t \]

signal <- 2*cos(2*pi*(1:n+15)/50)

x <- signal + rnorm(n)

tibble(t = 1:n, x = x, signal = signal) %>%

ggplot(aes(t, x)) +

geom_line() +

geom_line(aes(y = signal), color = "blue", linetype = "dashed")

Definición:

\[ \gamma(s,t) = \text{cov}(x_s, x_t) = E[(x_s - \mu_s)(x_t - \mu_t)] \]

\[ \gamma_w(s,t) = \begin{cases} \sigma_w^2 & s=t \\ 0 & s \neq t \end{cases} \]

Propiedad: Combinaciones Lineales

Si \(U=\sum a_j X_j\), \(V=\sum b_k Y_k\) son combinaciones lineales de series \(X_j\) e \(Y_k\) con varianza finita entonces:

\[ \text{cov}(U,V) = \sum_{j,k} a_j b_k \text{cov}(X_j, Y_k) \]

\[ \gamma_v(s,t)= \begin{cases} \frac{3}{9}\sigma_w^2 & s=t \\ \frac{2}{9}\sigma_w^2 & |s-t|=1 \\ \frac{1}{9}\sigma_w^2 & |s-t|=2 \\ 0 & |s-t|>2 \end{cases} \]

\[ x_t = \sum_{j=1}^t w_j \]

Definición:

\[ \rho(s,t) = \frac{\gamma(s,t)}{\sqrt{\gamma(s,s)\gamma(t,t)}} \]

Definición:

\[ \gamma_{xy}(s,t) = E[(x_s - \mu_{xs})(y_t - \mu_{yt})] \]

Definición:

\[ \rho_{xy}(s,t) = \frac{\gamma_{xy}(s,t)}{\sqrt{\gamma_x(s,s)\gamma_y(t,t)}} \]

Para el caso en donde tenemos \(r\) series:

\[ \gamma_{jk}(s,t) = E[(x_{sj} - \mu_{sj})(x_{tk} - \mu_{tk})], \quad j,k=1,\ldots,r \]

Notas:

Una serie \(\{x_t\}\) es estrictamente estacionaria si, para todo \(k\), cualquier conjunto de tiempos \(t_1, \dots, t_k\), cualquier conjunto de constantes \(c_1, \dots, c_k\), y cualquier corrimiento \(h\), se cumple:

\[ \Pr\{x_{t_1} \leq c_1, \dots, x_{t_k} \leq c_k\} = \Pr\{x_{t_1+h} \leq c_1, \dots, x_{t_k+h} \leq c_k\} \]

Casos particulares - \(k=1\):

\[

\Pr\{x_s \leq c\} = \Pr\{x_t \leq c\}

\] \(\implies\) La media \(\mu_t\) debe ser constante en \(t\).

Es decir, depende solo de la diferencia de tiempos.

Una serie \(\{x_t\}\) es débilmente estacionaria si:

En lo sucesivo, estacionaria se refiere a este caso.

Notación simplificada - Media: \[ \mu_t = \mu \] - Autocovarianza: \[ \gamma(h) = \mathrm{Cov}(x_{t+h}, x_t) = \mathbb{E}[(x_{t+h}-\mu)(x_t-\mu)] \] - Autocorrelación: \[ \rho(h) = \frac{\gamma(h)}{\gamma(0)} \]

Con \(-1 \leq \rho(h) \leq 1\).

\(\implies\) Estacionario débil.

Si además es normal, también es estrictamente estacionario: \(\rho_w(0)=1\), \(\rho_w(h)=0\) si \(h \neq 0\).

\(\mu_{vt}=0\)

\(\gamma_v(h)= \begin{cases} \frac{3}{9}\sigma_w^2 & h=0 \\ \frac{2}{9}\sigma_w^2 & h=\pm 1 \\ \frac{1}{9}\sigma_w^2 & h=\pm 2 \\ 0 & |h|>2 \end{cases}\)

\(\rho_v(h)= \begin{cases} 1 & h=0 \\ 2/3 & h=\pm 1 \\ 1/3 & h=\pm 2 \\ 0 & |h|>2 \end{cases}\)

\(\implies\) No estacionaria.

\(\implies\) No estacionaria en media, pero sí en la covarianza.

Se llama tendencia estacionaria.

No negatividad: \[ 0 \leq \operatorname{Var}(a_1x_1+\dots+a_nx_n) = \sum_{j=1}^n \sum_{k=1}^n a_j a_k \gamma(j-k) \]

Varianza: \[ \gamma(0)=\mathbb{E}[(x_t-\mu)^2] \]

Acotamiento: \[ |\gamma(h)| \leq \gamma(0) \]

Simetría: \[ \gamma(h)=\gamma(-h) \]

Dos series \(x_t\) y \(y_t\) son conjuntamente estacionarias si cada una es estacionaria y:

Función de covarianza cruzada: \[ \gamma_{xy}(h)=\operatorname{Cov}(x_{t+h}, y_t) \]

Función de correlación cruzada (CCF): \[ \rho_{xy}(h)=\frac{\gamma_{xy}(h)}{\sqrt{\gamma_x(0)\gamma_y(0)}} \]

Propiedades:

Con \(x_t = w_t+w_{t-1}\) y \(y_t = w_t-w_{t-1}\):

Entonces: \[ \rho_{xy}(h)= \begin{cases} 0 & h=0 \\ 1/2 & h=1 \\ -1/2 & h=-1 \\ 0 & |h|\geq 2 \end{cases} \]

\(\implies\) \(x_t\) y \(y_t\) son conjuntamente estacionarias.

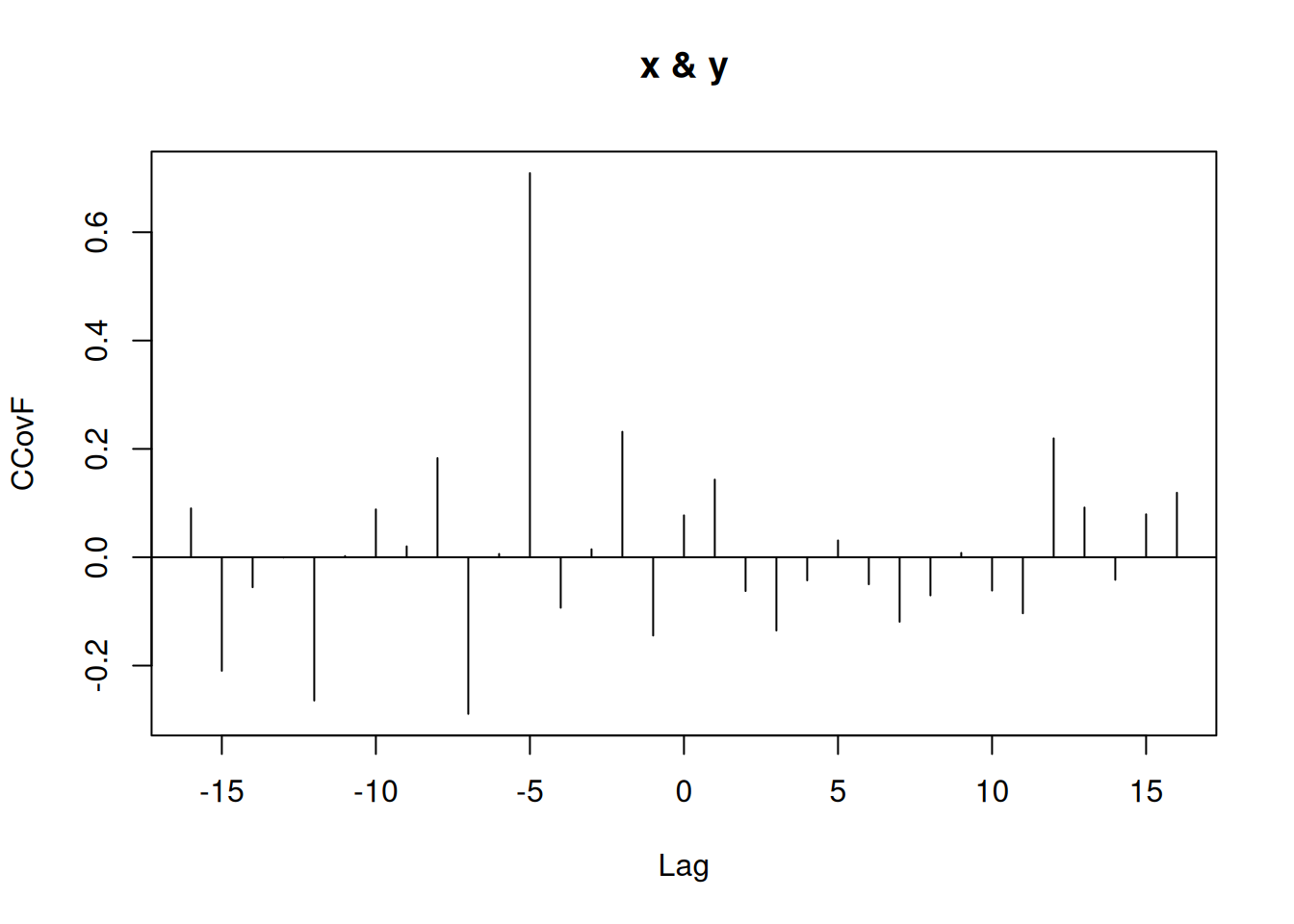

Si \(y_t = A x_{t-\ell} + w_t\) entonces \(x_t\) lidera a \(y_t\) si \(\ell>0\) y rezaga a \(y_t\) si \(\ell<0\).

Cálculo: \[ \gamma_{yx}(h) = A \gamma_x(h-\ell) \]

Se observa un pico en \(\gamma_{yx}(h)\) en \(h=\ell\).

Ejemplo en R

library(dplyr)

set.seed(123)

x <- rnorm(100)

y <- stats::lag(x, -5) + rnorm(100)

ccf(x, y, ylab = "CCovF", type = "covariance")

Definición:

\[ x_t = \mu + \sum_{j=-\infty}^\infty \psi_j w_{t-j}, \quad \sum_{j=-\infty}^\infty |\psi_j| < \infty \]

Autocovarianza:

\[ \gamma_x(h) = \sigma_w^2 \sum_{j=-\infty}^\infty \psi_{j+h}\psi_j \]

Definición: \({x_t}\) es Gaussiano si para cualquier conjunto de tiempos \(t_1,\dots,t_n\), el vector \((x_{t_1}, \dots, x_{t_n})'\) es multinormal con densidad:

\[ f(x)=(2\pi)^{-n/2}|\Gamma|^{-1/2}\exp\left\{-\tfrac{1}{2}(x-\mu)'\Gamma^{-1}(x-\mu)\right\} \]

Para una serie estacionaria, \(\mu_t = \mu\) es constante y puede estimarse con:

\[ \bar{x} = \frac{1}{n} \sum_{t=1}^n x_t \]

Varianza del estimador:

\[ \operatorname{var}(\bar{x}) = \frac{1}{n} \sum_{h=-n}^n \left(1-\frac{|h|}{n}\right) \gamma_x(h) \]

Definición Autocovarianza muestral:

\[ \hat{\gamma}(h) = n^{-1} \sum_{t=1}^{n-h} (x_{t+h}-\bar{x})(x_t-\bar{x}), \quad \hat{\gamma}(-h)=\hat{\gamma}(h) \]

Definición Autocorrelación muestral:

\[ \hat{\rho}(h) = \frac{\hat{\gamma}(h)}{\hat{\gamma}(0)} \]

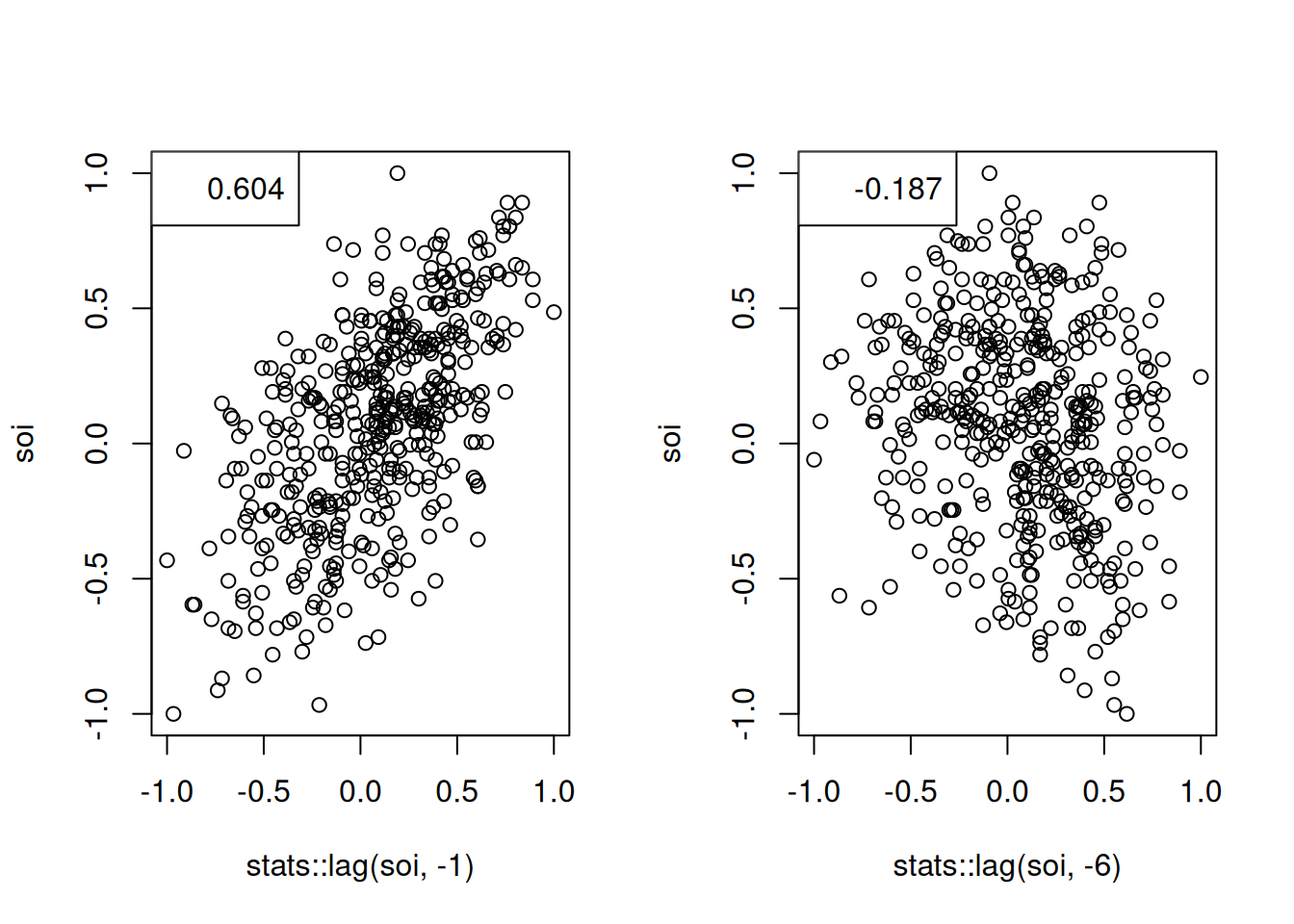

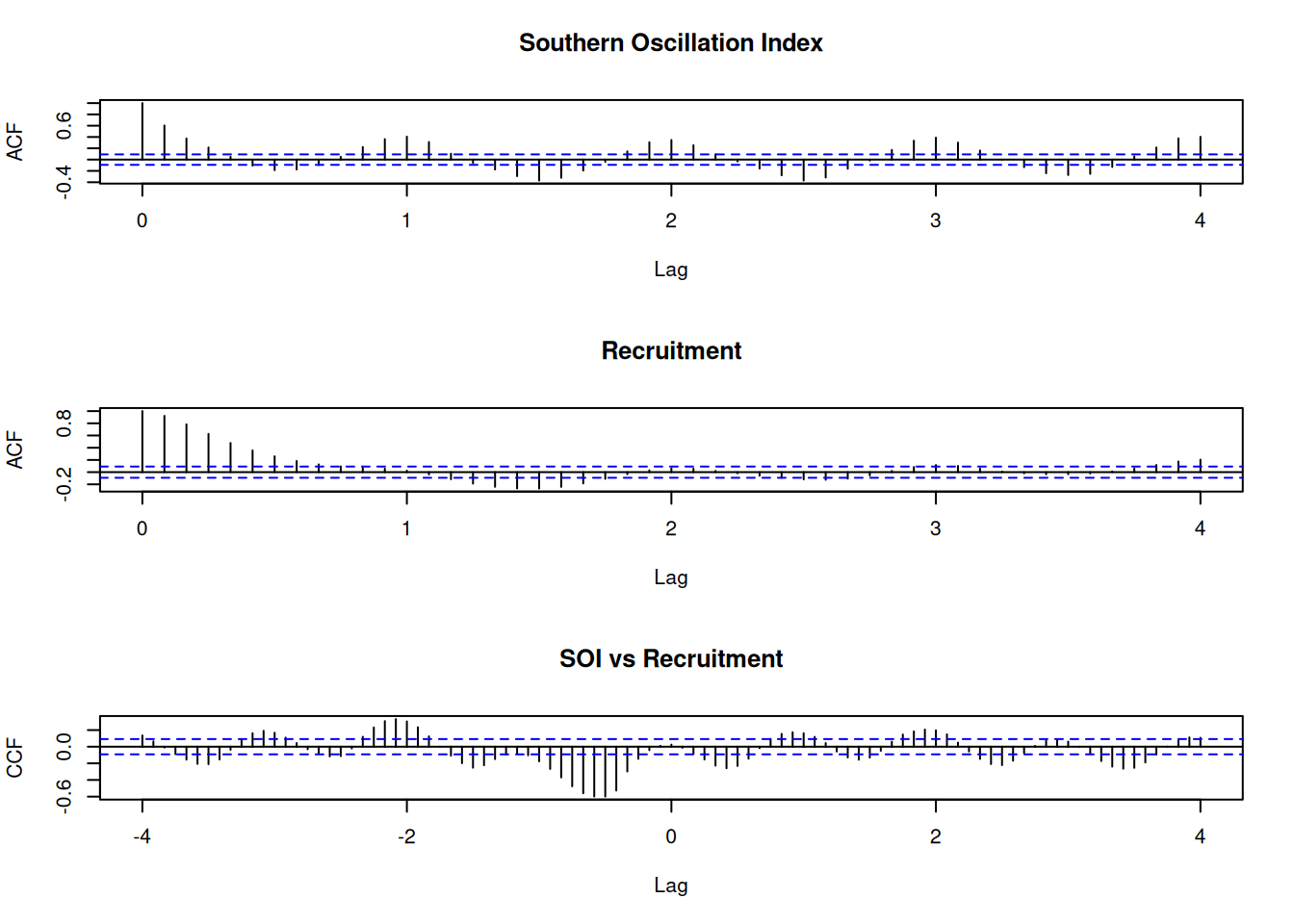

La estimación de \(\rho(h)\) se hace con pares \((x_t, x_{t+h})\). Ejemplo con la serie SOI:

r <- round(acf(soi, 6, plot=FALSE)$acf[-1], 3)

show(r)[1] 0.604 0.374 0.214 0.050 -0.107 -0.187par(mfrow=c(1,2))

plot(stats::lag(soi, -1), soi); legend("topleft", legend=r[1])

plot(stats::lag(soi, -6), soi); legend("topleft", legend=r[6])

Propiedad Distribución asintótica de la ACF

Si \(x_t\) es ruido blanco y \(n\) es grande:

\[ \hat{\rho}_x(h) \sim N(0, 1/n), \quad h=1,2,\dots,H \]

Criterio práctico: \(\hat{\rho}(h)\) es significativo si está fuera de \(\pm 2/\sqrt{n}\).

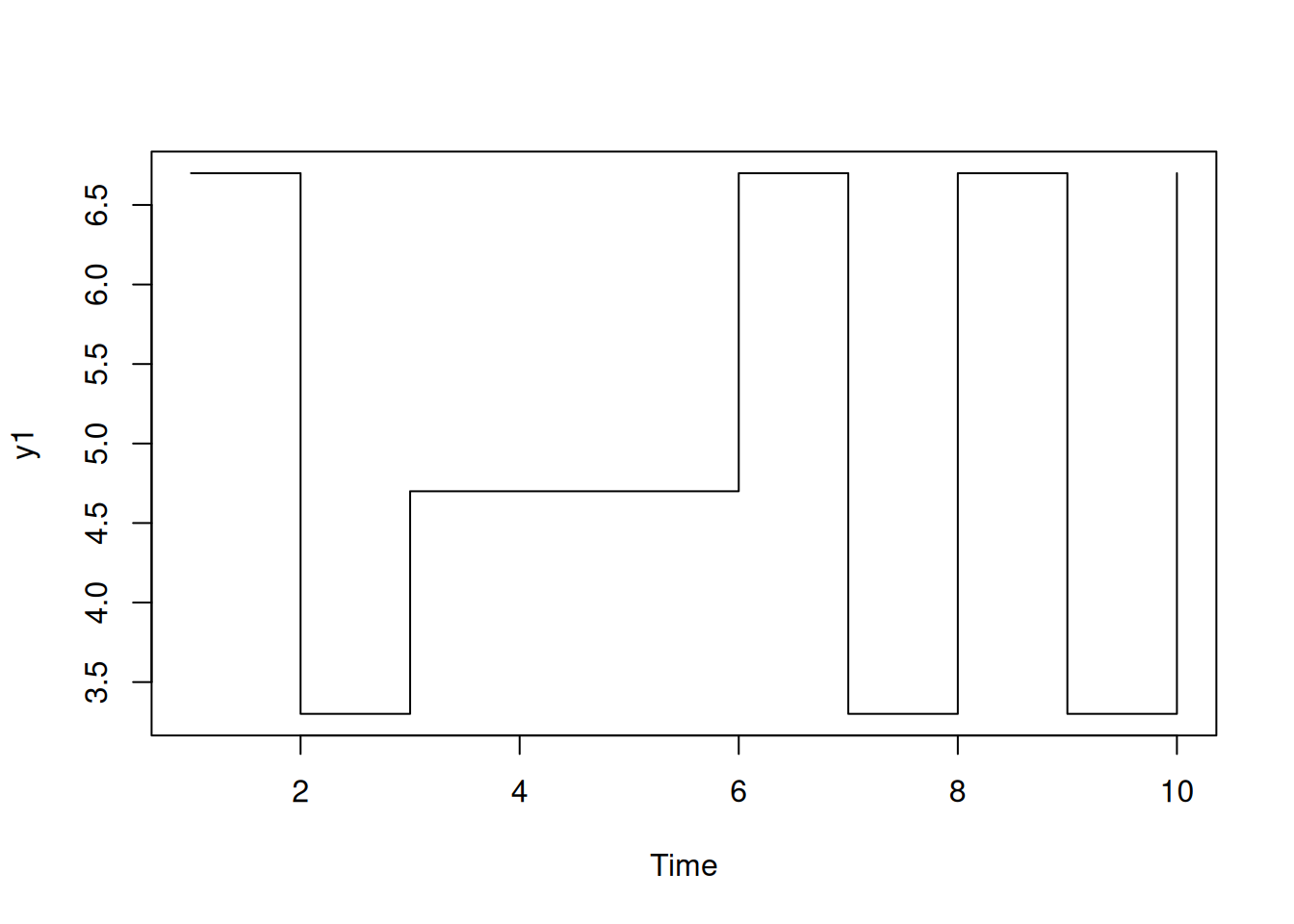

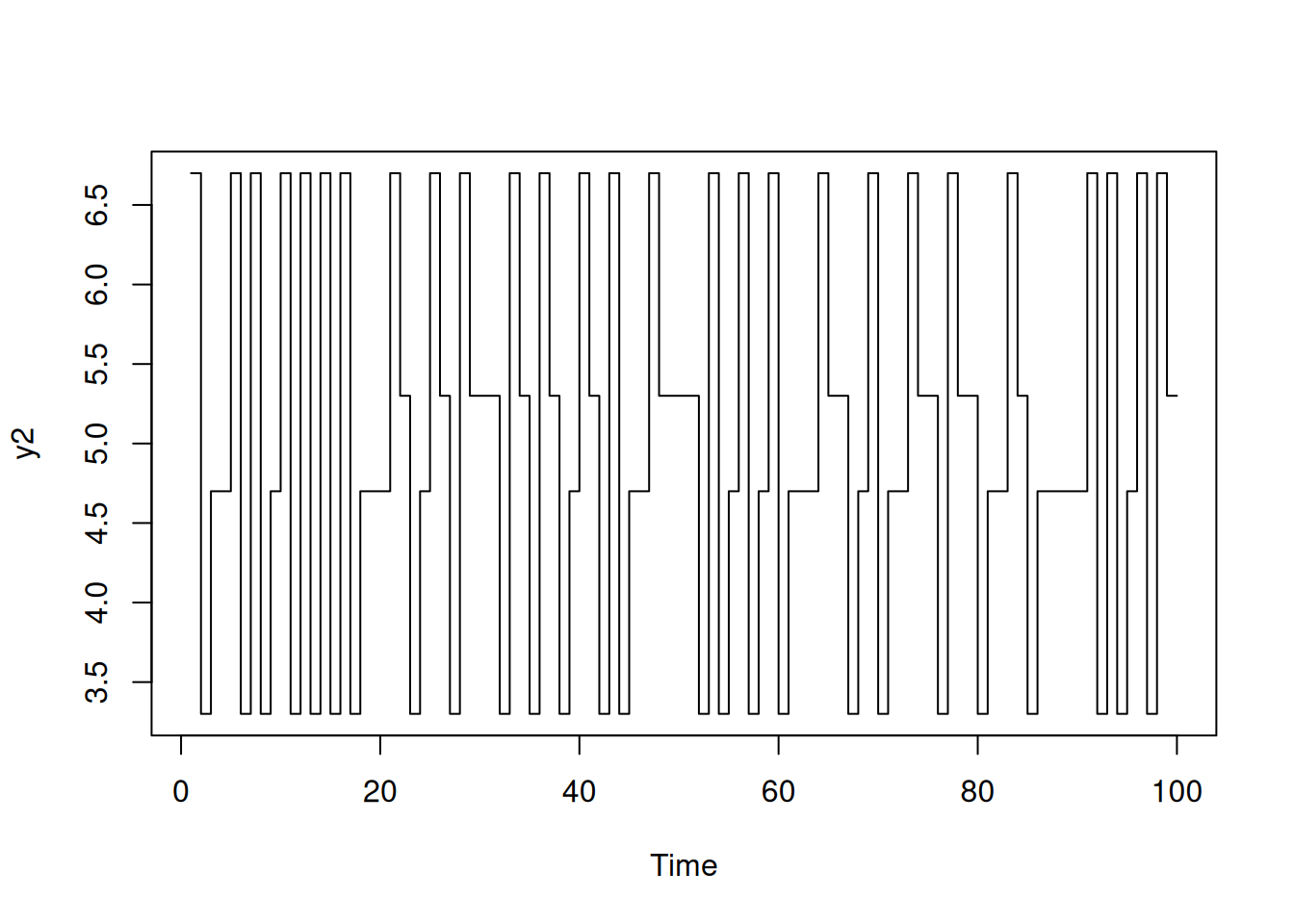

Modelo:

\[ y_t = 5 + x_t - 0.7 x_{t-1}, \quad x_t \in \{-1,1\} \]

Comparación con \(n=10\) y \(n=100\).

set.seed(101010)

x1 <- 2*rbinom(11, 1, .5) - 1

x2 <- 2*rbinom(101, 1, .5) - 1

y1 <- 5 + stats::filter(x1, sides=1, filter=c(1,-.7))[-1]

y2 <- 5 + stats::filter(x2, sides=1, filter=c(1,-.7))[-1]

plot.ts(y1, type="s")

plot.ts(y2, type="s")

c(mean(y1), mean(y2))[1] 5.080 5.002acf(y1, lag.max=4, plot=FALSE)

Autocorrelations of series 'y1', by lag

0 1 2 3 4

1.000 -0.688 0.425 -0.306 -0.007 acf(y2, lag.max=4, plot=FALSE)

Autocorrelations of series 'y2', by lag

0 1 2 3 4

1.000 -0.480 -0.002 -0.004 0.000 Teóricamente:

\[ \rho_y(1) = \frac{-0.7}{1+0.7^2} = -0.47, \quad \rho_y(h)=0 \text{ si } |h|>1 \]

Definición Covarianza cruzada muestral:

\[ \hat{\gamma}_{xy}(h) = n^{-1} \sum_{t=1}^{n-h} (x_{t+h}-\bar{x})(y_t-\bar{y}), \quad \hat{\gamma}_{xy}(-h)=\hat{\gamma}_{yx}(h) \]

Definición Correlación cruzada muestral:

\[ \hat{\rho}_{xy}(h) = \frac{\hat{\gamma}_{xy}(h)}{\sqrt{\hat{\gamma}_x(0)\hat{\gamma}_y(0)}} \]

Propiedad Distribución asintótica de la correlación cruzada

Si uno de los procesos es ruido blanco:

\[ \hat{\rho}_{xy}(h) \sim N(0, 1/n) \]

par(mfrow=c(3,1))

acf(soi, 48, main="Southern Oscillation Index")

acf(rec, 48, main="Recruitment")

ccf(soi, rec, 48, main="SOI vs Recruitment", ylab="CCF")

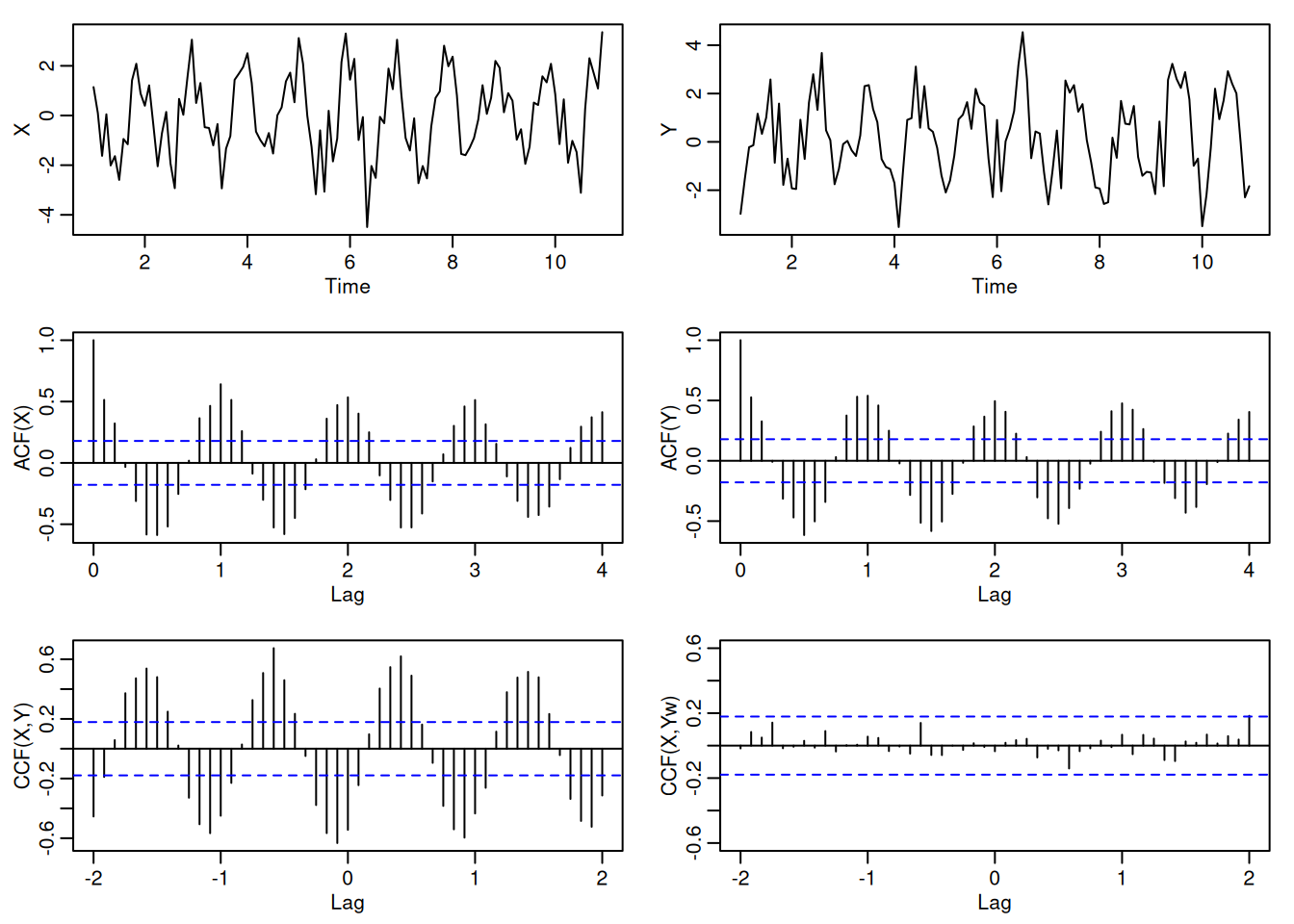

Generación de dos series independientes con comportamiento cíclico:

\[ x_t = 2\cos\left(2\pi t/12\right) + w_{t1}, \quad y_t = 2\cos\left(2\pi (t+5)/12\right) + w_{t2} \]

El preblanqueo elimina la señal de \(y_t\) ajustando regresión con \(\cos\) y \(\sin\).

set.seed(1492)

num <- 120; t <- 1:num

X <- ts(2*cos(2*pi*t/12) + rnorm(num), freq=12)

Y <- ts(2*cos(2*pi*(t+5)/12) + rnorm(num), freq=12)

Yw <- resid(lm(Y ~ cos(2*pi*t/12) + sin(2*pi*t/12), na.action=NULL))

par(mfrow=c(3,2), mgp=c(1.6,.6,0), mar=c(3,3,1,1))

plot(X); plot(Y)

acf(X,48, ylab="ACF(X)")

acf(Y,48, ylab="ACF(Y)")

ccf(X,Y,24, ylab="CCF(X,Y)")

ccf(X,Yw,24, ylab="CCF(X,Yw)", ylim=c(-.6,.6))

Sea \(x_t = (x_{t1}, x_{t2}, \ldots, x_{tp})'\) un vector de \(p\) series de tiempo.

\[ \mu = \mathbb{E}(x_t) \]

\[ \Gamma(h) = \mathbb{E}\left[(x_{t+h}-\mu)(x_t-\mu)'\right] \]

\[ \gamma_{ij}(h) = \mathbb{E}[(x_{t+h,i}-\mu_i)(x_{tj}-\mu_j)] \]

\[ \Gamma(-h) = \Gamma'(h) \]

\[ \hat{\Gamma}(h) = \frac{1}{n}\sum_{t=1}^{n-h} (x_{t+h}-\bar{x})(x_t-\bar{x})' \]

\[ \bar{x} = \frac{1}{n} \sum_{t=1}^n x_t \]

\[ \hat{\Gamma}(-h) = \hat{\Gamma}(h)' \]

Un proceso \(x_s\) puede estar indexado por un vector de coordenadas espaciales/temporales \(s=(s_1, s_2, \ldots, s_r)'\).

\[ \gamma(h) = \mathbb{E}[(x_{s+h}-\mu)(x_s-\mu)] \]

\[ \mu = \mathbb{E}(x_s) \]

En el caso bidimensional (\(r=2\)):

\[ \gamma(h_1,h_2) = \mathbb{E}[(x_{s_1+h_1,s_2+h_2}-\mu)(x_{s_1,s_2}-\mu)] \]

\[ \hat{\gamma}(h) = (S_1 S_2 \cdots S_r)^{-1} \sum_{s_1}\sum_{s_2}\cdots\sum_{s_r} (x_{s+h}-\bar{x})(x_s-\bar{x}) \]

\[ \bar{x} = (S_1 S_2 \cdots S_r)^{-1}\sum_{s_1}\sum_{s_2}\cdots\sum_{s_r} x_{s_1,s_2,\dots,s_r} \]

\[ \hat{\rho}(h) = \frac{\hat{\gamma}(h)}{\hat{\gamma}(0)} \]

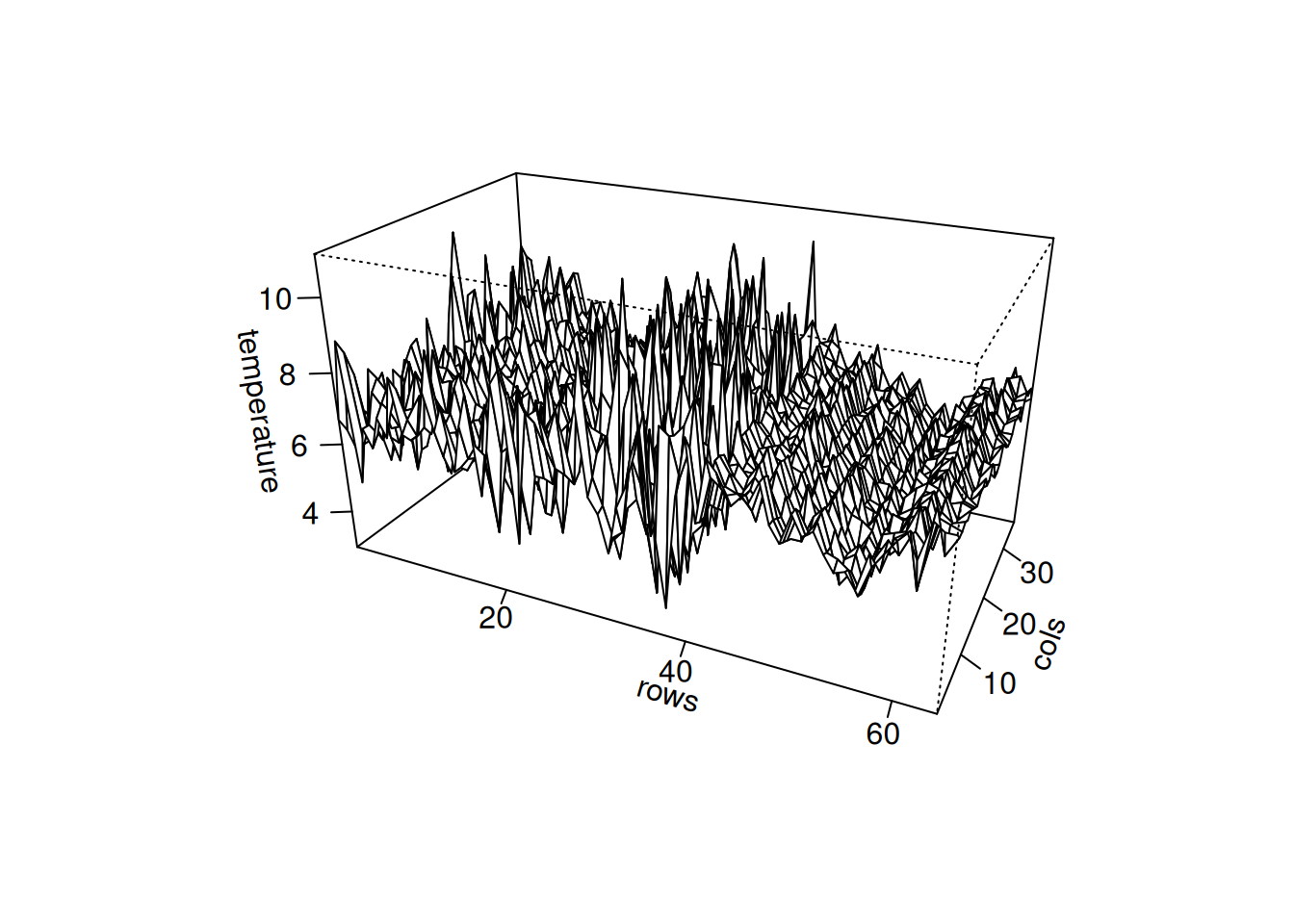

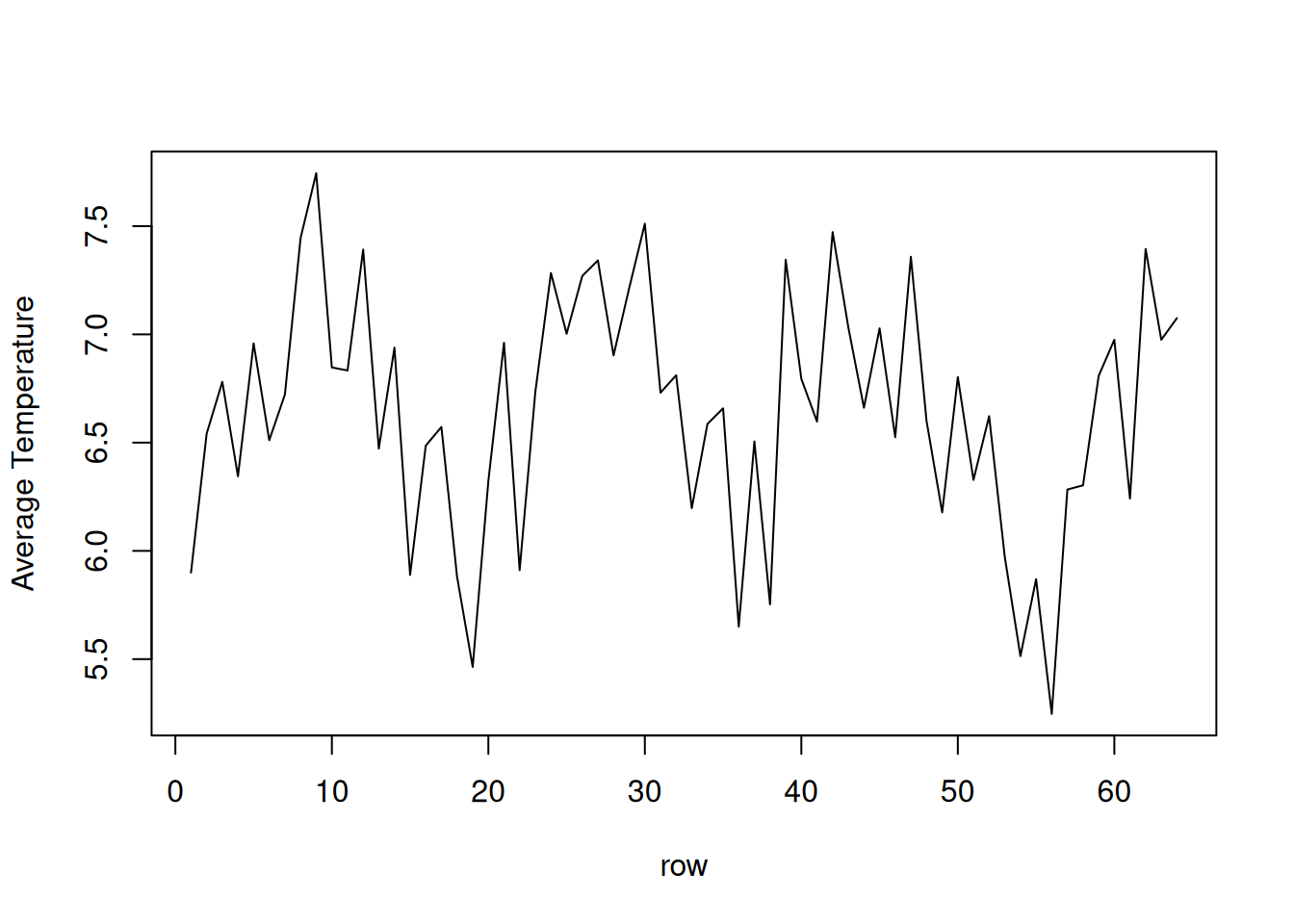

Serie de temperaturas medidas en una grilla \(64 \times 36\). Se observa un cambio a partir de la fila 40, con oscilaciones más estables y periódicas.

Cálculo de promedios por fila:

persp(1:64, 1:36, soiltemp, phi=25, theta=25, scale=FALSE,

expand=4, ticktype="detailed",

xlab="rows", ylab="cols", zlab="temperature")

plot.ts(rowMeans(soiltemp), xlab="row", ylab="Average Temperature")

\[ \hat{\rho}(h_1,h_2) = \frac{\hat{\gamma}(h_1,h_2)}{\hat{\gamma}(0,0)} \]

con

\[ \hat{\gamma}(h_1,h_2) = (S_1 S_2)^{-1}\sum_{s_1}\sum_{s_2}(x_{s_1+h_1,s_2+h_2}-\bar{x})(x_{s_1,s_2}-\bar{x}) \]

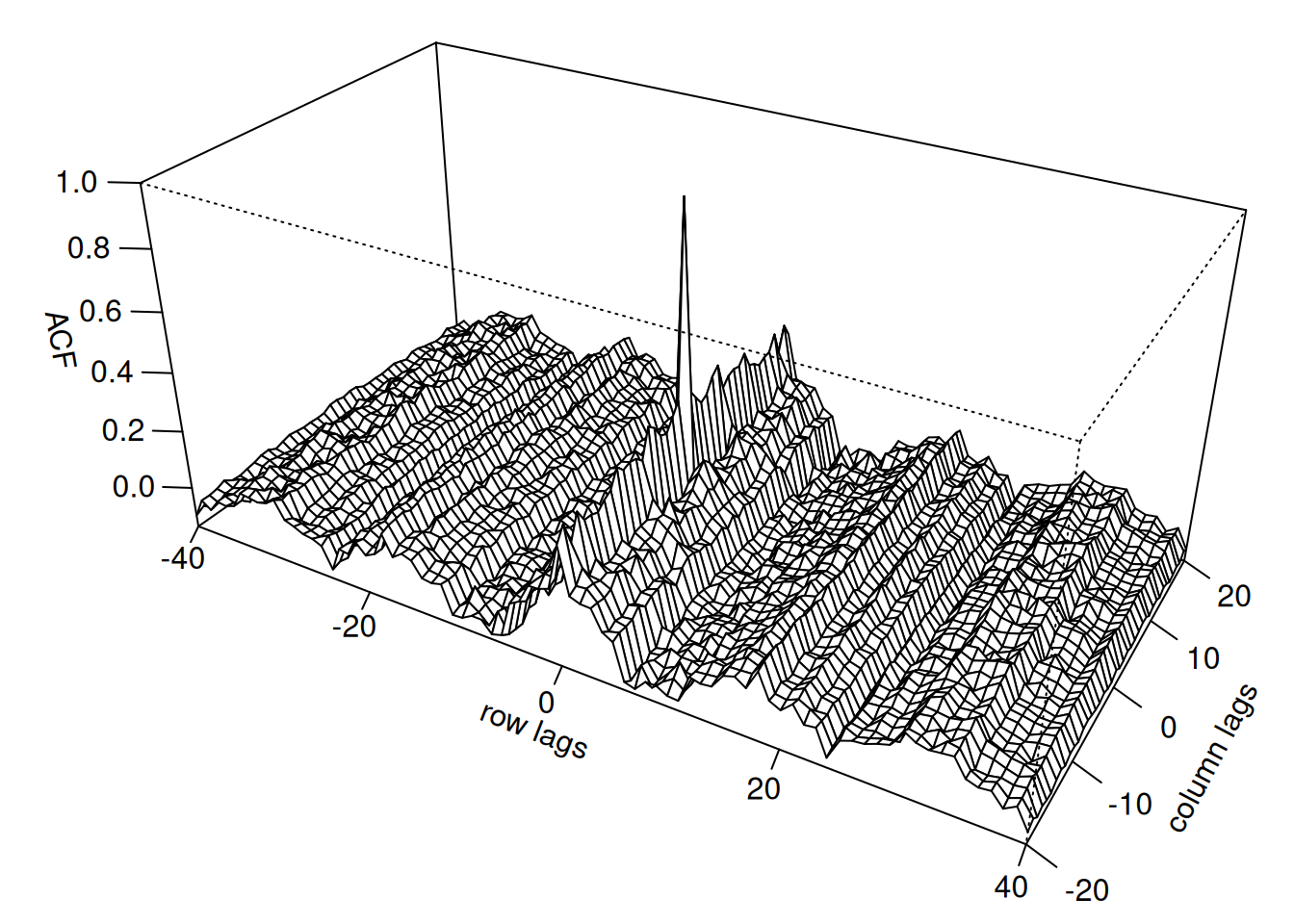

fs <- Mod(fft(soiltemp - mean(soiltemp)))^2/(64*36)

cs <- Re(fft(fs, inverse=TRUE)/sqrt(64*36)) # ACovF

rs <- cs/cs[1,1] # ACF

rs2 <- cbind(rs[1:41,21:2], rs[1:41,1:21])

rs3 <- rbind(rs2[41:2,], rs2)

par(mar=c(1,2.5,0,0)+.1)

persp(-40:40, -20:20, rs3, phi=30, theta=30, expand=30, scale="FALSE",

ticktype="detailed", xlab="row lags", ylab="column lags",

zlab="ACF")

En casos de observaciones irregulares se utiliza el variograma:

\[ 2V_x(h) = \operatorname{Var}(x_{s+h}-x_s) \]

\[ 2\hat{V}_x(h) = \frac{1}{N(h)} \sum_s (x_{s+h}-x_s)^2 \]

donde \(N(h)\) es el número de puntos en el vecindario de \(h\).