5.1.1 Modelo base y problema de sobrediferenciación

Sea el proceso AR(1) causal (ruido gaussiano): \[

x_t=\phi x_{t-1}+w_t.

\]

Aplicando \((1-B)\) a ambos lados: \[

\nabla x_t=\phi \nabla x_{t-1}+\nabla w_t,\quad

y_t=\phi y_{t-1}+w_t-w_{t-1},

\] donde \(y_t=\nabla x_t\). Así, \(y_t\) es un ARMA\((1,1)\) no invertible: diferenciar puede introducir correlación espuria y problemas de invertibilidad.

Bajo una caminata aleatoria \(x_t=x_{t-1}+w_t\) con \(x_0=0\) y \(\mu_x=0\), el estimador LS es \[

\hat{\phi}=\frac{\sum_{t=1}^{n} x_t x_{t-1}}{\sum_{t=1}^{n} x_{t-1}^2}

=1+\frac{\frac{1}{n}\sum_{t=1}^{n} w_t x_{t-1}}{\frac{1}{n}\sum_{t=1}^{n} x_{t-1}^2}.

\] Por tanto, \[

\hat{\phi}-1=\frac{\frac{1}{n\sigma_w^2}\sum_{t=1}^{n} w_t x_{t-1}}

{\frac{1}{n\sigma_w^2}\sum_{t=1}^{n} x_{t-1}^2}.

\]

Dado \(x_t=x_{t-1}+w_t\), se tiene \(x_t^2=x_{t-1}^2+2x_{t-1}w_t+w_t^2\), luego \[

x_{t-1}w_t=\tfrac{1}{2}\left(x_t^2-x_{t-1}^2-w_t^2\right),

\] y al sumar, \[

\frac{1}{n\sigma_w^2}\sum_{t=1}^{n}x_{t-1}w_t

=\frac{1}{2}\left(\frac{x_n^2}{n\sigma_w^2}-\frac{\sum_{t=1}^{n}w_t^2}{n\sigma_w^2}\right).

\] Como \(x_n=\sum_{1}^{n}w_t\sim N(0,n\sigma_w^2)\), entonces \(\chi_1^2=\frac{x_n^2}{n\sigma_w^2}\) y \(\frac{1}{n}\sum_{1}^{n}w_t^2\to_p \sigma_w^2\). En consecuencia, \[

\frac{1}{n\sigma_w^2}\sum_{t=1}^{n}x_{t-1}w_t \xrightarrow{d} \tfrac{1}{2}\left(\chi_1^2-1\right).

\]

5.1.3 Movimiento browniano estándar

Un proceso continuo \({W(t);t\ge 0}\) es browniano estándar si:

\(W(0)=0\);

incrementos independientes en puntos \(0\le t_1<\cdots<t_n\);

\(W(t+\Delta t)-W(t)\sim N(0,\Delta t)\) para \(\Delta t>0\), con trayectorias casi seguramente continuas.

5.1.3.1 Teorema central funcional

Si \(\xi_1,\ldots,\xi_n\) iid con media 0 y varianza 1, para \(0\le t\le 1\): \[

S_n(t)=\frac{1}{\sqrt{n}}\sum_{j=1}^{[[ nt]]}\xi_j \xrightarrow{d} W(t).

\] Bajo \(H_0\), \(x_s=w_1+\cdots+w_s\sim N(0,s\sigma_w^2)\) y \(\frac{x_s}{\sigma_w\sqrt{n}}\xrightarrow{d}W(s)\). Por tanto, \[

\sum_{t=1}^{n}\left(\frac{x_{t-1}}{\sigma_w\sqrt{n}}\right)^2\frac{1}{n}

\xrightarrow{d}\int_{0}^{1}W^2(t),dt.

\]

5.1.4 Estadístico DF y su límite

Ajustando el factor \(n^{-1}\) del denominador de la expresión de \(\hat \phi-1\):

\[

n(\hat{\phi}-1)=

\frac{\frac{1}{n\sigma_w^2}\sum_{t=1}^{n} w_t x_{t-1}}

{\frac{1}{n^{2}\sigma_w^2}\sum_{t=1}^{n} x_{t-1}^{2}}

\xrightarrow{d}\frac{\tfrac{1}{2}\left(\chi_1^2-1\right)}

{\int_{0}^{1}W^2(t),dt}.

\] Este es el estadístico de Dickey–Fuller (DF). Su distribución no tiene forma cerrada; los cuantiles se obtienen por aproximación numérica o simulación.

5.1.5 Extensiones DF/ADF/PP

Reescribiendo \(x_t=\phi x_{t-1}+w_t\) como \(\nabla x_t=\gamma x_{t-1}+w_t\) con \(\gamma=\phi-1\), se prueba \(H_0:\gamma=0\) por regresión de \(\nabla x_t\) sobre \(x_{t-1}\). Para AR(\(p\)): \[

\nabla x_t=\gamma x_{t-1}+\sum_{j=1}^{p-1}\psi_j \nabla x_{t-j}+w_t,

\] donde \(\gamma=\sum_{j=1}^{p}\phi_j-1\) y \(\psi_j=-\sum_{i=j}^{p}\phi_i\) para \(j=2,\ldots,p\). El ADF contrasta \(H_0:\gamma=0\) vía \(t_\gamma=\hat\gamma/\operatorname{se}(\hat\gamma)\) en la regresión sobre \(x_{t-1},\nabla x_{t-1},\ldots,\nabla x_{t-p+1}\). Para ARMA\((p,q)\) se usa ADF con \(p\) grande o el test de Phillips–Perron (PP), que trata de forma distinta la correlación serial y heterocedasticidad en los errores.

5.1.5.1 Ejemplo: Pruebas de raíz unitaria en la serie de varves glaciares

A continuación se usan pruebas DF, ADF y PP sobre el logaritmo de la serie de varves glaciares (cada prueba incluye constante y tendencia lineal). En ADF, el número de retardos AR \(k\) por defecto es \([[(n-1)^{1/3}]]\); en PP, \(k=[[ 0.04n^{1/4}]]\).

library(tidyverse)

── Attaching core tidyverse packages ──────────────────────── tidyverse 2.0.0 ──

✔ dplyr 1.1.4 ✔ readr 2.1.5

✔ forcats 1.0.0 ✔ stringr 1.5.2

✔ ggplot2 4.0.0 ✔ tibble 3.3.0

✔ lubridate 1.9.4 ✔ tidyr 1.3.1

✔ purrr 1.1.0

── Conflicts ────────────────────────────────────────── tidyverse_conflicts() ──

✖ dplyr::filter() masks stats::filter()

✖ dplyr::lag() masks stats::lag()

ℹ Use the conflicted package (<http://conflicted.r-lib.org/>) to force all conflicts to become errors

library(astsa)library(tseries)

Registered S3 method overwritten by 'quantmod':

method from

as.zoo.data.frame zoo

adf.test(log(varve), k =0) # DF

Warning in adf.test(log(varve), k = 0): p-value smaller than printed p-value

Augmented Dickey-Fuller Test

data: log(varve)

Dickey-Fuller = -12.857, Lag order = 0, p-value = 0.01

alternative hypothesis: stationary

adf.test(log(varve)) # ADF (k por defecto)

Augmented Dickey-Fuller Test

data: log(varve)

Dickey-Fuller = -3.5166, Lag order = 8, p-value = 0.04071

alternative hypothesis: stationary

pp.test(log(varve)) # PP

Warning in pp.test(log(varve)): p-value smaller than printed p-value

Phillips-Perron Unit Root Test

data: log(varve)

Dickey-Fuller Z(alpha) = -304.54, Truncation lag parameter = 6, p-value

= 0.01

alternative hypothesis: stationary

5.2 Modelos GARCH

5.2.1 Modelado de volatilidad: retornos y motivación

Si \(x_t\) es el valor del activo en \(t\), el retorno relativo es \[

r_t=\frac{x_t-x_{t-1}}{x_{t-1}}.

\] Como \(x_t=(1+r_t)x_{t-1}\), si el cambio porcentual es pequeño: \[

\nabla\log(x_t)\approx r_t.

\] Usaremos indistintamente \(r_t\equiv \nabla\log(x_t)\) o \((x_t-x_{t-1})/x_{t-1}\).

5.2.2 Modelo ARCH(1): definición y propiedades

5.2.2.1 Especificación básica

\[

\begin{aligned}

r_t&=\sigma_t\epsilon_t, \\

\sigma_t^2&=\alpha_0+\alpha_1 r_{t-1}^2,

\end{aligned}

\] con \(\epsilon_t\sim \text{iid }N(0,1)\) y \(\alpha_0,\alpha_1\ge 0\).

La distribución condicional: \[

r_t\mid r_{t-1}\sim N\left(0,\ \alpha_0+\alpha_1 r_{t-1}^2\right).

\]

5.2.2.2 Representación para \(r_t^2\)

A partir de la definición del modelo ARCH: \[

\begin{aligned}

r_t^2 &= \sigma_t^2 \, \epsilon_t^2, \\

\alpha_0 + \alpha_1 r_{t-1}^2 &= \sigma_t^2,

\end{aligned}

\] y restando ambas ecuaciones se obtiene:

\[

r_t^2 - \left( \alpha_0 + \alpha_1 r_{t-1}^2 \right) = \sigma_t^2 (\epsilon_t^2 - 1),

\] de donde se obtiene:

\[

r_t^2=\alpha_0+\alpha_1 r_{t-1}^2+v_t,\quad v_t=\sigma_t^2(\epsilon_t^2-1),

\] donde \(\epsilon_t^2-1\) es \(\chi_1^2\) desplazada o centrada en 0.

Propiedades

Sea \(\mathcal{R}_s=\{r_s,r_{s-1},\ldots\}\). Entonces \[

\mathrm{E}(r_t)=\mathrm{E}[{\mathrm{E}(r_t\mid \mathcal{R}_{t-1})}]

=\mathrm{E}[{\mathrm{E}(r_t\mid r_{t-1})}]=0,

\] por lo tanto es una diferencia martingala y para \(h>0\), \[

\operatorname{cov}(r_{t+h},r_t)=\mathrm{E}{r_t\mathrm{E}(r_{t+h}\mid\mathcal{R}_{t+h-1})}=0.

\]

Si \(0\le \alpha_1<1\) y \(\operatorname{var}(v_t)\) es finita y constante entonces \(r_t^2\) es AR(1) causal (estacionario), por lo que \[

\mathrm{E}(r_t^2)=\operatorname{var}(r_t)=\frac{\alpha_0}{1-\alpha_1},

\] y \[

\mathrm{E}(r_t^4)=\frac{3\alpha_0^2}{(1-\alpha_1)^2}\cdot \frac{1-\alpha_1^2}{1-3\alpha_1^2},\quad (3\alpha_1^2<1).

\] La curtosis es \[

\kappa=\frac{\mathrm{E}(r_t^4)}{[\mathrm{E}(r_t^2)]^2}=3\frac{1-\alpha_1^2}{1-3\alpha_1^2}\ge 3,

\] lo que indica colas pesadas (leptocurtosis). Si \(3\alpha_1^2<1\), \(\rho_{r^2}(h)=\alpha_1^h\ge 0\).

5.2.3 Estimación por verosimilitud condicional

La verosimilitud condicional de \(r_2,\ldots,r_n\) dado \(r_1\) es \[

L(\alpha_0,\alpha_1\mid r_1)=\prod_{t=2}^n f_{\alpha_0,\alpha_1}(r_t\mid r_{t-1}),

\] y el criterio a minimizar es \[

l(\alpha_0,\alpha_1)=\tfrac{1}{2}\sum_{t=2}^n \ln(\alpha_0+\alpha_1 r_{t-1}^2)

+\tfrac{1}{2}\sum_{t=2}^n \frac{r_t^2}{\alpha_0+\alpha_1 r_{t-1}^2}.

\] El MLE solamente se obtiene por métodos numéricos. Para esto se necesita el gradiente: \[

\binom{\partial l/\partial \alpha_0}{\partial l/\partial \alpha_1}

=\sum_{t=2}^n \binom{1}{r_{t-1}^2}

\frac{\alpha_0+\alpha_1 r_{t-1}^2-r_t^2}{2(\alpha_0+\alpha_1 r_{t-1}^2)^2}.

\]

Nota: la logverosimilitud para este tipo de modelo tiende a ser muy plana.

También es posible combinar un modelo de regresión con errores ARCH:

\[

x_t=\beta^t z_t+y_t

\] donde \(y_t\) es ARCH. En particular un AR(1) podría tener errores ARCH:

\[

\sigma_t^2=\alpha_0+\alpha_1 r_{t-1}^2+\beta_1 \sigma_{t-1}^2,

\] y si \(\alpha_1+\beta_1<1\), \[

r_t^2=\alpha_0+(\alpha_1+\beta_1) r_{t-1}^2+v_t-\beta_1 v_{t-1}.

\] donde \(v_t\) se definió anteriormente.

La estimación de máxima verosimilitud condicional de los parámetros del modelo GARCH\((p,q)\) es similar al caso ARCH\((p)\), en el cual la verosimilitud condicional es el producto de densidades \(\mathrm{N}(0, \sigma_t^2)\) con \(\sigma_t^2\) dado por la ecuación anterior, y donde la condición se establece sobre las primeras \(\max(p,q)\) observaciones, con \(\sigma_1^2 = \cdots = \sigma_q^2 = 0\). Una vez que se obtienen las estimaciones de los parámetros, el modelo puede utilizarse para obtener pronósticos de volatilidad de un paso adelante, denotados como \(\hat{\sigma}_{t+1}^2\), dados por

En series financieras (y otras), la varianza condicional puede cambiar en el tiempo: periodos de alta volatilidad tienden a agruparse. Los modelos ARCH/GARCH modelan esa heterocedasticidad condicional.

Sea \({\varepsilon_t}\) la secuencia de residuos (por ejemplo, de un modelo para la media). Decimos que hay efecto ARCH de orden \(q\) si la varianza condicional en \(t\) depende de los cuadrados de los últimos \(q\) residuos: \[

\operatorname{Var}(\varepsilon_t\mid \mathcal F_{t-1}) = \alpha_0 + \alpha_1\varepsilon_{t-1}^2 + \cdots + \alpha_q\varepsilon_{t-q}^2,

\quad \alpha_0>0, \alpha_j\ge 0.

\]

La prueba LM ARCH (Engle) contrasta:

\(H_0\): no hay efecto ARCH (varianza condicional constante; \(\alpha_1=\cdots=\alpha_q=0\)).

\(H_1\): sí hay efecto ARCH de algún orden (\(\exists j:\alpha_j\ne 0\)).

Regresión auxiliar y estadístico

La prueba se implementa ajustando la regresión sobre los residuos al cuadrado: \[

\hat{\varepsilon}_t^2 =\alpha_0+\alpha_1\hat{\varepsilon}_{t-1}^2+\cdots+\alpha_q \hat{\varepsilon}_{t-q}^2+u_t.

\]

Sea \(R^2\) el coeficiente de determinación de esta regresión y \(n\) el número de observaciones usadas. El estadístico LM es: \[

\text{LM}=nR^2 \overset{H_0}{\approx}\chi^2_q.

\]

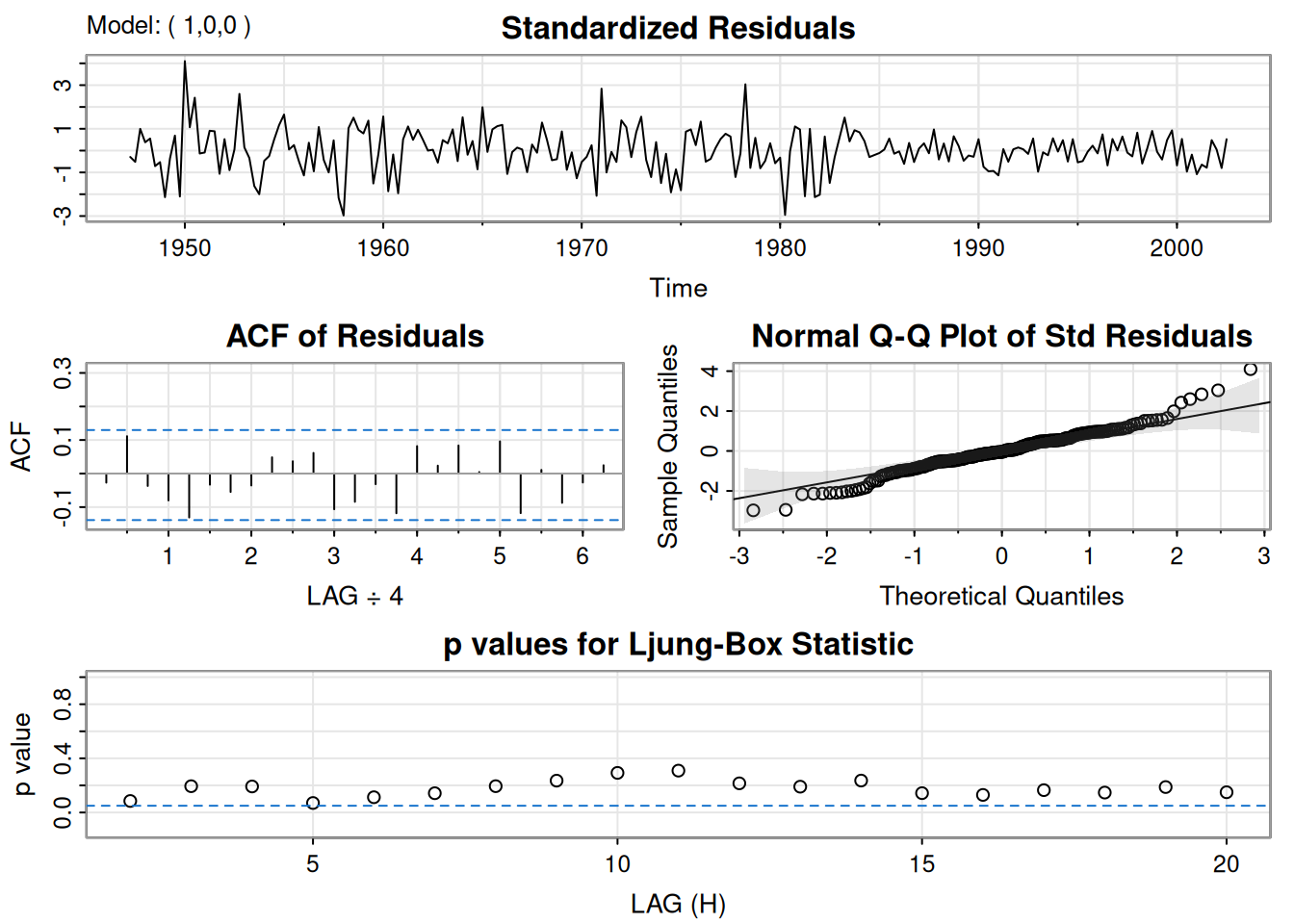

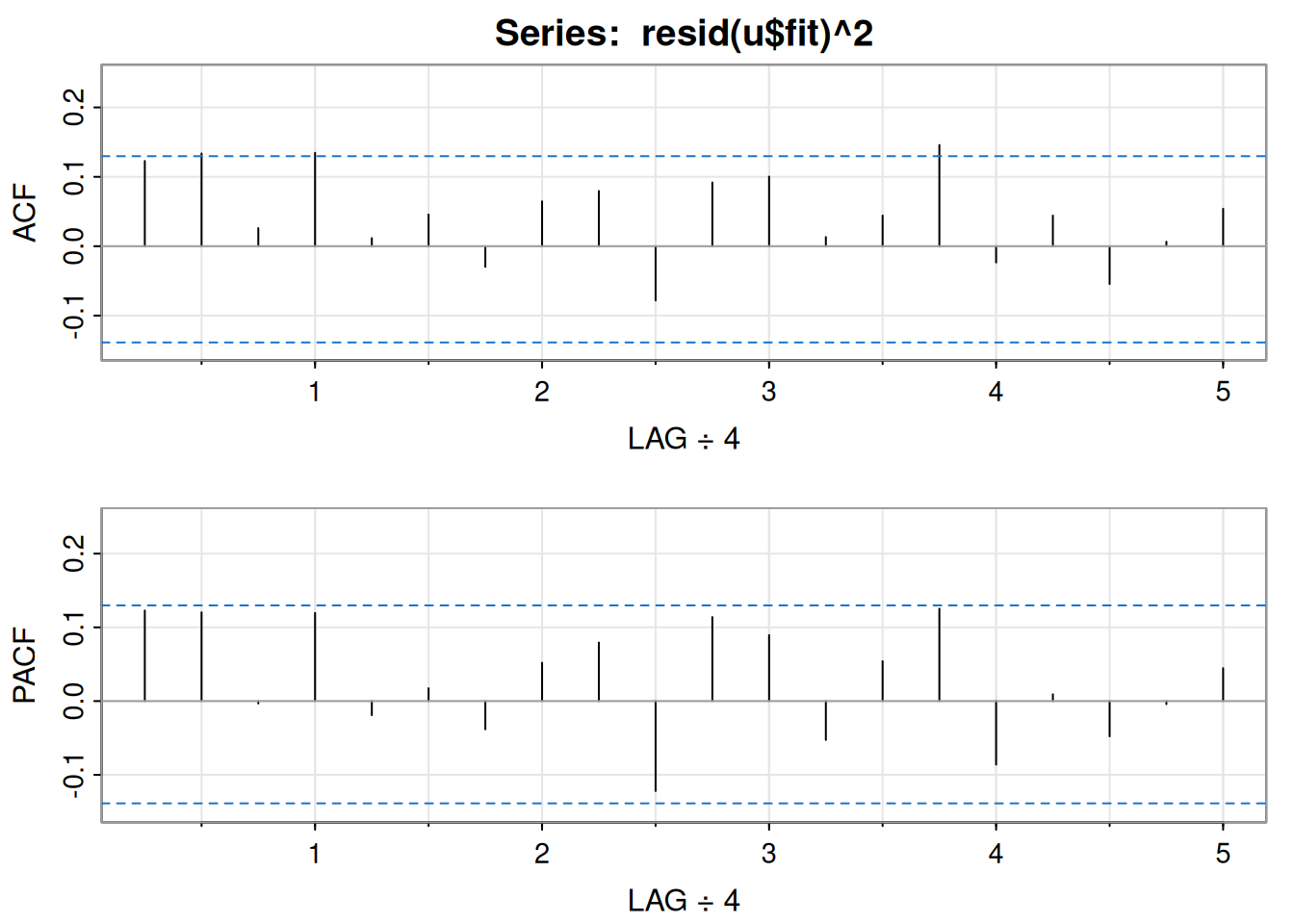

5.2.5.1 Ejemplo: Análisis ARCH en U.S. GNP

La ACF/PACF de los cuadrados de los residuales del AR(1) sugiere dependencia débil.

u =sarima(diff(log(gnp)), 1, 0, 0)

initial value -4.589567

iter 2 value -4.654150

iter 3 value -4.654150

iter 4 value -4.654151

iter 4 value -4.654151

iter 4 value -4.654151

final value -4.654151

converged

initial value -4.655919

iter 2 value -4.655921

iter 3 value -4.655922

iter 4 value -4.655922

iter 5 value -4.655922

iter 5 value -4.655922

iter 5 value -4.655922

final value -4.655922

converged

<><><><><><><><><><><><><><>

Coefficients:

Estimate SE t.value p.value

ar1 0.3467 0.0627 5.5255 0

xmean 0.0083 0.0010 8.5398 0

sigma^2 estimated as 9.029569e-05 on 220 degrees of freedom

AIC = -6.44694 AICc = -6.446693 BIC = -6.400958

NOTE: Packages 'fBasics', 'timeDate', and 'timeSeries' are no longer

attached to the search() path when 'fGarch' is attached.

If needed attach them yourself in your R script by e.g.,

require("timeSeries")

Series Initialization:

ARMA Model: arma

Formula Mean: ~ arma(1, 0)

GARCH Model: garch

Formula Variance: ~ garch(1, 0)

ARMA Order: 1 0

Max ARMA Order: 1

GARCH Order: 1 0

Max GARCH Order: 1

Maximum Order: 1

Conditional Dist: norm

h.start: 2

llh.start: 1

Length of Series: 222

Recursion Init: mci

Series Scale: 0.01015924

Parameter Initialization:

Initial Parameters: $params

Limits of Transformations: $U, $V

Which Parameters are Fixed? $includes

Parameter Matrix:

U V params includes

mu -8.20681904 8.206819 0.8205354 TRUE

ar1 -0.99999999 1.000000 0.3466459 TRUE

omega 0.00000100 100.000000 0.1000000 TRUE

alpha1 0.00000001 1.000000 0.1000000 TRUE

gamma1 -0.99999999 1.000000 0.1000000 FALSE

delta 0.00000000 2.000000 2.0000000 FALSE

skew 0.10000000 10.000000 1.0000000 FALSE

shape 1.00000000 10.000000 4.0000000 FALSE

Index List of Parameters to be Optimized:

mu ar1 omega alpha1

1 2 3 4

Persistence: 0.1

--- START OF TRACE ---

Selected Algorithm: nlminb

R coded nlminb Solver:

0: 682.89527: 0.820535 0.346646 0.100000 0.100000

1: 308.43148: 0.763492 0.258112 1.06104 0.352453

2: 306.07332: 0.681276 0.195897 1.04763 0.304072

3: 301.00807: 0.561958 0.448458 0.825277 0.0402737

4: 298.88361: 0.383716 0.465477 0.632947 0.385969

5: 296.74288: 0.504144 0.389445 0.683635 0.247795

6: 296.67703: 0.497724 0.366843 0.688130 0.229496

7: 296.60039: 0.500011 0.385702 0.703145 0.211105

8: 296.59692: 0.515646 0.374174 0.690079 0.194961

9: 296.56381: 0.513570 0.367018 0.702272 0.200013

10: 296.55723: 0.523440 0.363126 0.708406 0.194151

11: 296.55632: 0.522578 0.364913 0.710104 0.194839

12: 296.55598: 0.520871 0.364956 0.710924 0.193212

13: 296.55568: 0.519486 0.366571 0.710212 0.194511

14: 296.55568: 0.519509 0.366597 0.710266 0.194512

15: 296.55568: 0.519511 0.366585 0.710290 0.194451

16: 296.55568: 0.519505 0.366562 0.710299 0.194464

17: 296.55568: 0.519526 0.366560 0.710295 0.194472

18: 296.55568: 0.519522 0.366563 0.710295 0.194471

Final Estimate of the Negative LLH:

LLH: -722.2849 norm LLH: -3.253536

mu ar1 omega alpha1

0.0052779470 0.3665625656 0.0000733096 0.1944713341

R-optimhess Difference Approximated Hessian Matrix:

mu ar1 omega alpha1

mu -2749495.418 -24170.124984 4.546826e+06 -1.586692e+03

ar1 -24170.125 -390.266822 1.253879e+04 -6.733789e+00

omega 4546825.784 12538.791045 -1.590043e+10 -7.069342e+05

alpha1 -1586.692 -6.733789 -7.069342e+05 -1.425395e+02

attr(,"time")

Time difference of 0.004799604 secs

--- END OF TRACE ---

Time to Estimate Parameters:

Time difference of 0.02542353 secs

Title:

GARCH Modelling

Call:

garchFit(formula = ~arma(1, 0) + garch(1, 0), data = diff(log(gnp)))

Mean and Variance Equation:

data ~ arma(1, 0) + garch(1, 0)

<environment: 0x55c60f614660>

[data = diff(log(gnp))]

Conditional Distribution:

norm

Coefficient(s):

mu ar1 omega alpha1

0.00527795 0.36656257 0.00007331 0.19447133

Std. Errors:

based on Hessian

Error Analysis:

Estimate Std. Error t value Pr(>|t|)

mu 5.278e-03 8.996e-04 5.867 4.44e-09 ***

ar1 3.666e-01 7.514e-02 4.878 1.07e-06 ***

omega 7.331e-05 9.011e-06 8.135 4.44e-16 ***

alpha1 1.945e-01 9.554e-02 2.035 0.0418 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Log Likelihood:

722.2849 normalized: 3.253536

Description:

Tue Oct 28 15:18:41 2025 by user:

Standardised Residuals Tests:

Statistic p-Value

Jarque-Bera Test R Chi^2 9.1180362 0.010472337

Shapiro-Wilk Test R W 0.9842406 0.014336495

Ljung-Box Test R Q(10) 9.8743260 0.451587525

Ljung-Box Test R Q(15) 17.5585456 0.286584404

Ljung-Box Test R Q(20) 23.4136291 0.268943681

Ljung-Box Test R^2 Q(10) 19.2821015 0.036822455

Ljung-Box Test R^2 Q(15) 33.2364834 0.004352735

Ljung-Box Test R^2 Q(20) 37.7425917 0.009518989

LM Arch Test R TR^2 25.4162474 0.012969006

Information Criterion Statistics:

AIC BIC SIC HQIC

-6.471035 -6.409726 -6.471669 -6.446282

# Nota: garch(1,0) ≡ ARCH(1) en este código.

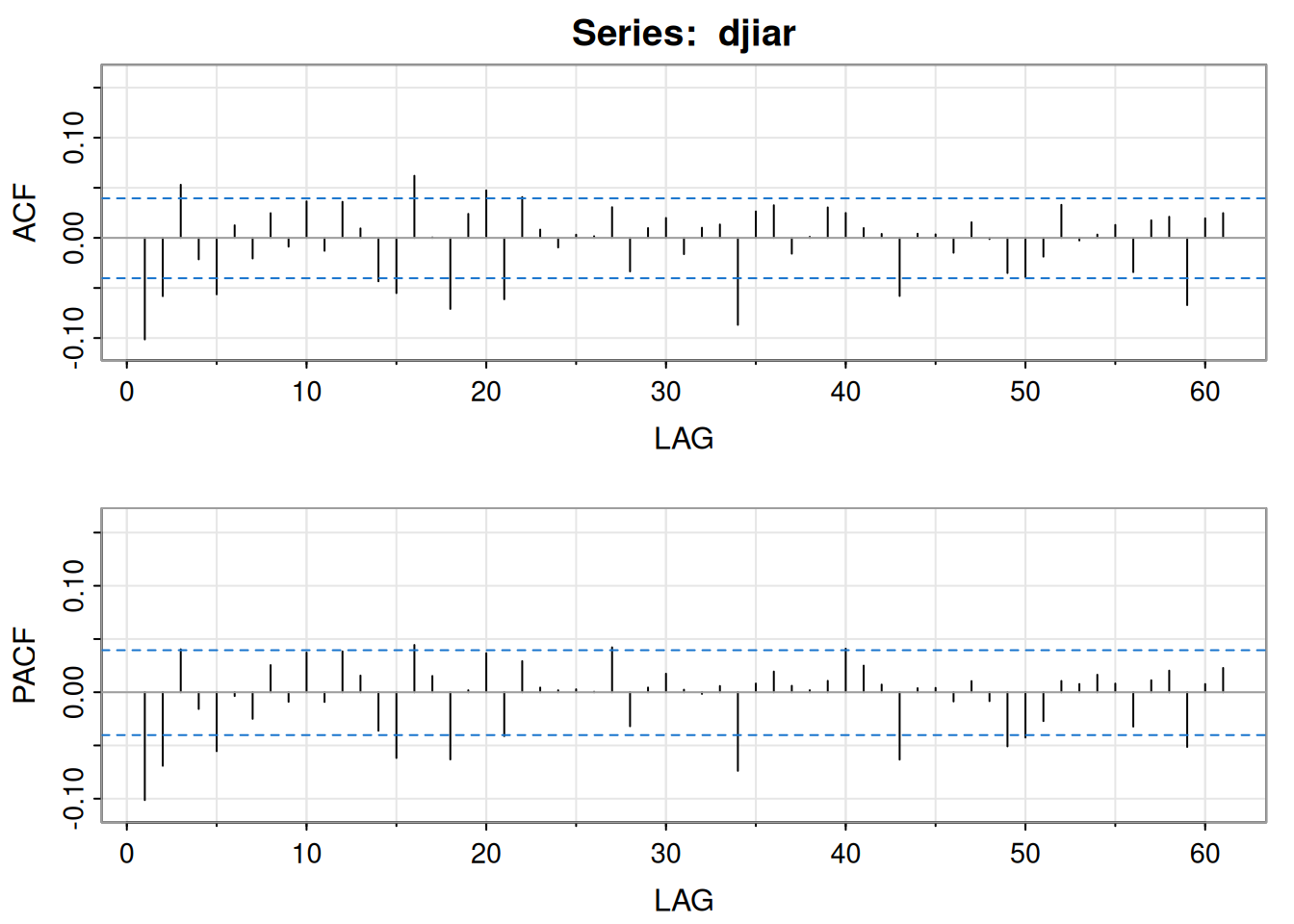

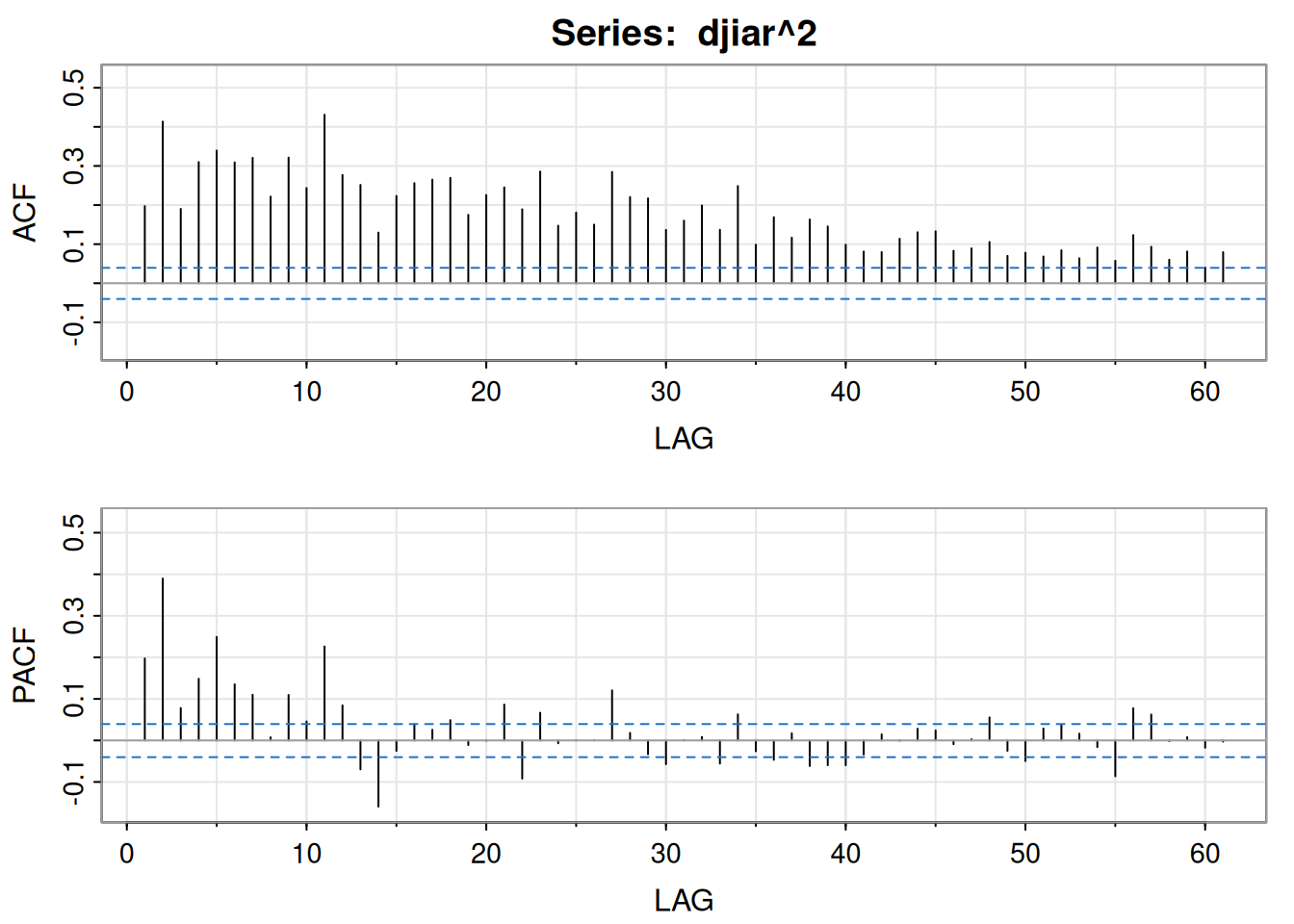

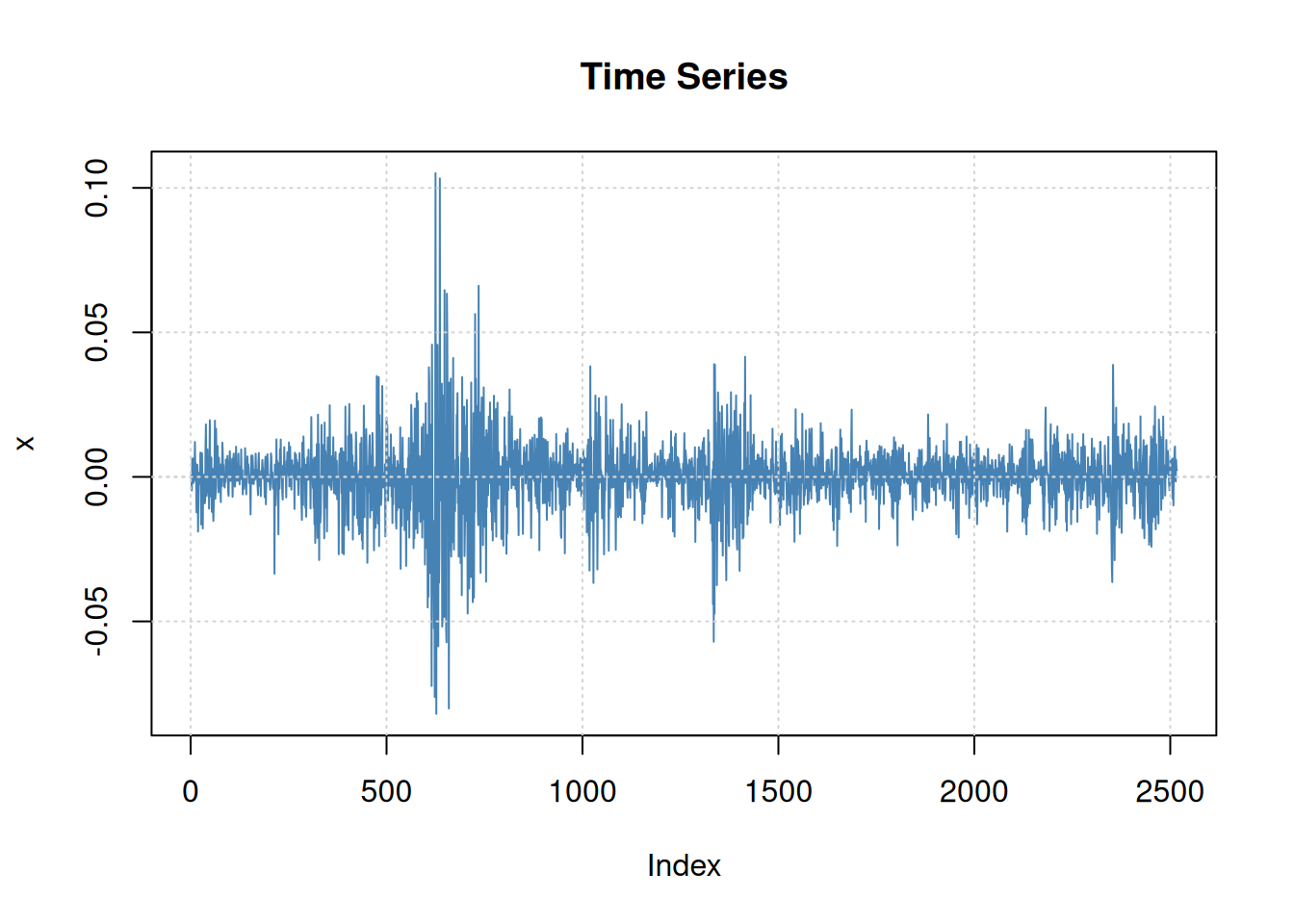

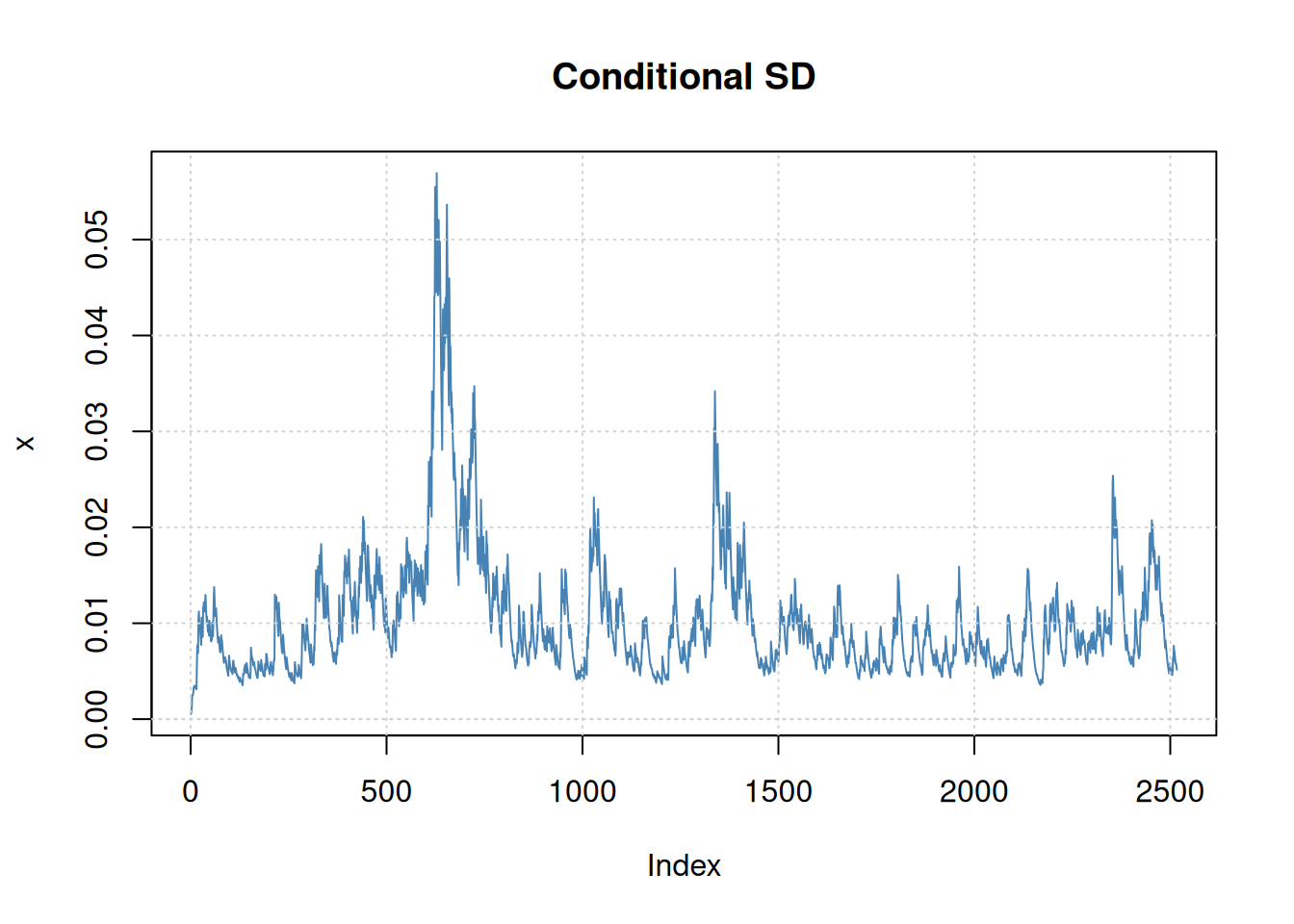

5.2.5.2 Ejemplo: Análisis GARCH del retorno DJIA

En este caso se usa errores t-Student para capturar colas un poco más pesadas(ver Manual fGarch):

library(xts)

Loading required package: zoo

Attaching package: 'zoo'

The following objects are masked from 'package:base':

as.Date, as.Date.numeric

######################### Warning from 'xts' package ##########################

# #

# The dplyr lag() function breaks how base R's lag() function is supposed to #

# work, which breaks lag(my_xts). Calls to lag(my_xts) that you type or #

# source() into this session won't work correctly. #

# #

# Use stats::lag() to make sure you're not using dplyr::lag(), or you can add #

# conflictRules('dplyr', exclude = 'lag') to your .Rprofile to stop #

# dplyr from breaking base R's lag() function. #

# #

# Code in packages is not affected. It's protected by R's namespace mechanism #

# Set `options(xts.warn_dplyr_breaks_lag = FALSE)` to suppress this warning. #

# #

###############################################################################

Attaching package: 'xts'

The following objects are masked from 'package:dplyr':

first, last

djiar =diff(log(djia$Close))[-1]acf2(djiar) # autocorrelación baja (no mostrado)

Modelo de potencia asimétrico ARCH con varianza condicional:

\[

\sigma_t^\delta=\alpha_0+\sum_{j=1}^p \alpha_j\left(\lvert r_{t-j}\rvert-\gamma_j r_{t-j}\right)^\delta

+\sum_{j=1}^q \beta_j \sigma_{t-j}^\delta,

\] Nótese que el modelo es GARCH cuando \(\delta = 2\) y \(\gamma_j = 0\), para \(j \in \{1, \ldots, p\}\). Los parámetros \(\gamma_j\) (\(|\gamma_j| \leq 1\)) son los parámetros de apalancamiento (leverage), que representan una medida de asimetría, y \(\delta > 0\) es el parámetro del término de potencia.

Un valor positivo [negativo] de \(\gamma_j\) significa que los choques negativos [positivos] pasados tienen un impacto más fuerte en la volatilidad condicional actual que los choques positivos [negativos] pasados. Este modelo combina la flexibilidad de un exponente variable con el coeficiente de asimetría para tener en cuenta el efecto de apalancamiento.

Además, para garantizar que \(\sigma_t > 0\), se asume que \(\alpha_0 > 0\), \(\alpha_j \geq 0\) (con al menos un \(\alpha_j > 0\)) y \(\beta_j \geq 0\).

5.2.6.1 Continuación del ejemplo del DJIA:

Siempre con errores t-Student:

library(xts)library(fGarch)summary(djia.ap <-garchFit(~arma(1,0) +aparch(1,1), data = djiar,cond.dist ='std'))

En GARCH, \(\sigma_t^2\) es determinística condicionalmente. El modelo de volatilidad estocástica introduce aleatoriedad: \[

r_t=\sigma_t \epsilon_t \ \Rightarrow\ \log r_t^2=\log \sigma_t^2+\log \epsilon_t^2

\] y la volatilidad latente sigue \[

\log \sigma_{t+1}^2=\phi_0+\phi_1 \log \sigma_t^2+w_t,\quad w_t\sim \text{iid }N(0,\sigma_w^2).

\] El objetivo es estimar \(\phi_0,\phi_1,\sigma_w^2\) y predecir la volatilidad futura.

5.3 Modelos de Umbral (Threshold Models)

Para una serie temporal estacionaria, la mejor predicción lineal hacia adelante es igual a la mejor predicción lineal hacia atrás. Esto se debe a que la matriz de varianza-covarianza \(\Gamma = {\gamma(i-j)}_{i,j=1}^n\) es simétrica y los procesos gaussianos tienen distribuciones idénticas al invertirse en el tiempo. Sin embargo, muchas series reales no cumplen esta propiedad: por ejemplo, las muertes por influenza aumentan más rápido de lo que disminuyen, mostrando asimetrías y no estacionalidad perfecta.

5.3.1 Modelos TARMA (Threshold ARMA)

Una alternativa no lineal es el modelo TARMA (Threshold ARMA), que ajusta modelos lineales locales en distintos regímenes. Un modelo SETARMA (Self-Exciting Threshold ARMA) de \(k\) regímenes se define como:

donde \(w_t^{(j)} \sim \text{iid } N(0, \sigma_j^2)\) para \(j = 1, \ldots, k\), \(d\) es un retardo, y \(r_1 < \cdots < r_{k-1}\) son los umbrales que dividen los regímenes.

Cada régimen corresponde a un modelo ARMA diferente, y las condiciones de estacionariedad e invertibilidad dependen de las propiedades de cada régimen.

Extensiones del modelo

El umbral puede depender de valores pasados del proceso o de variables exógenas. En ese caso, puede sustituirse \(x_{t-d}\) por otra variable \(y_{t-d}\) que represente tales variables.

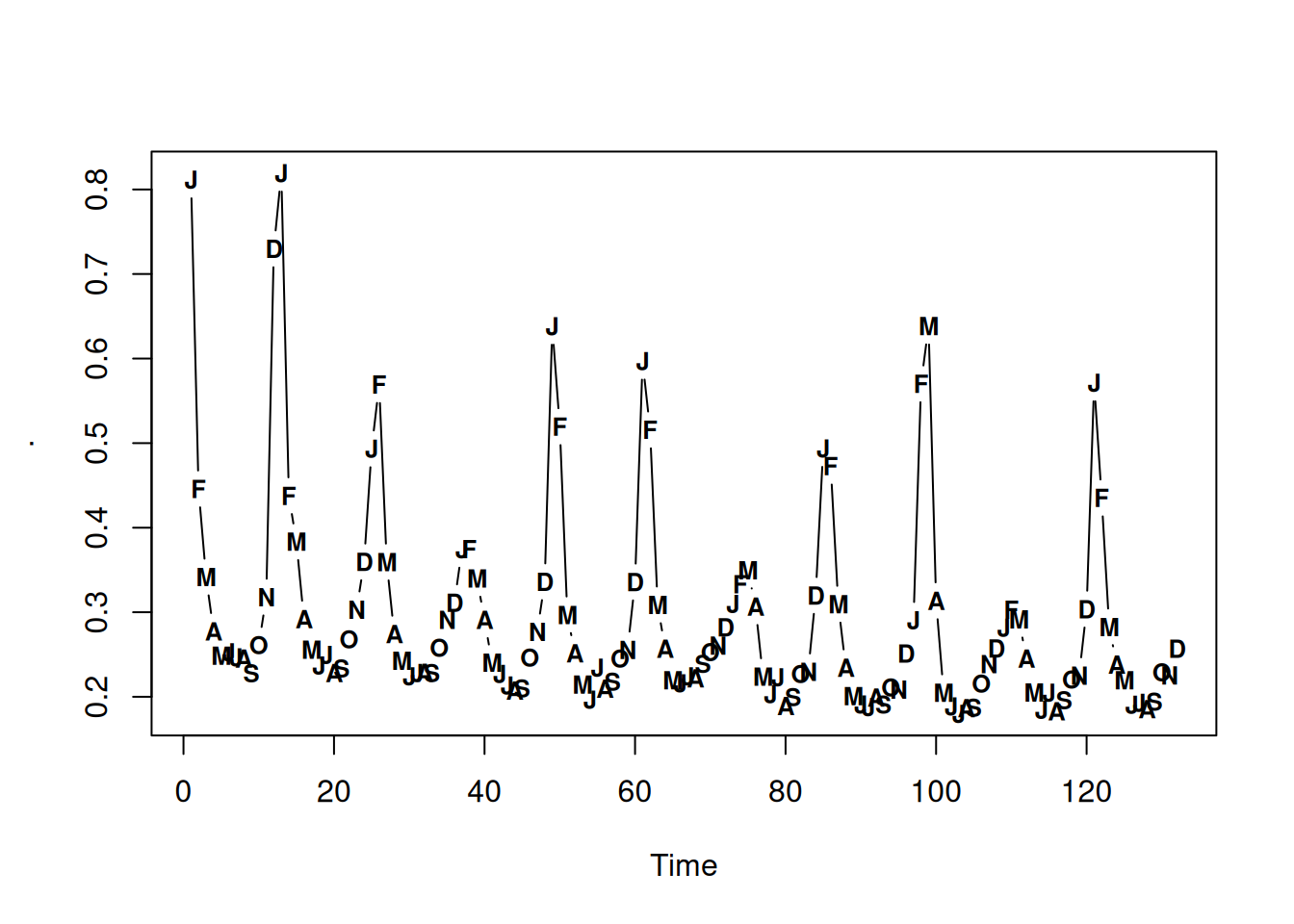

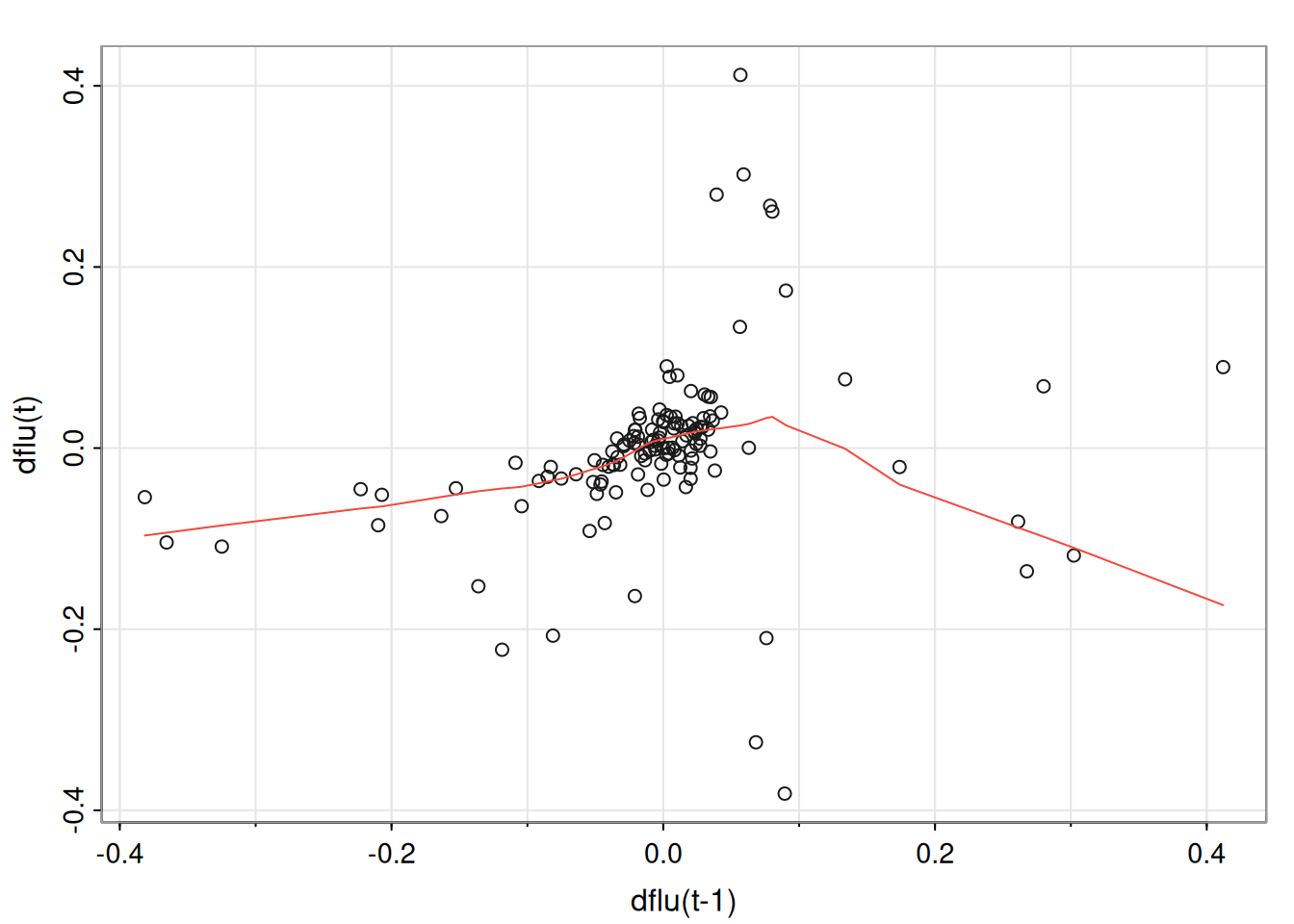

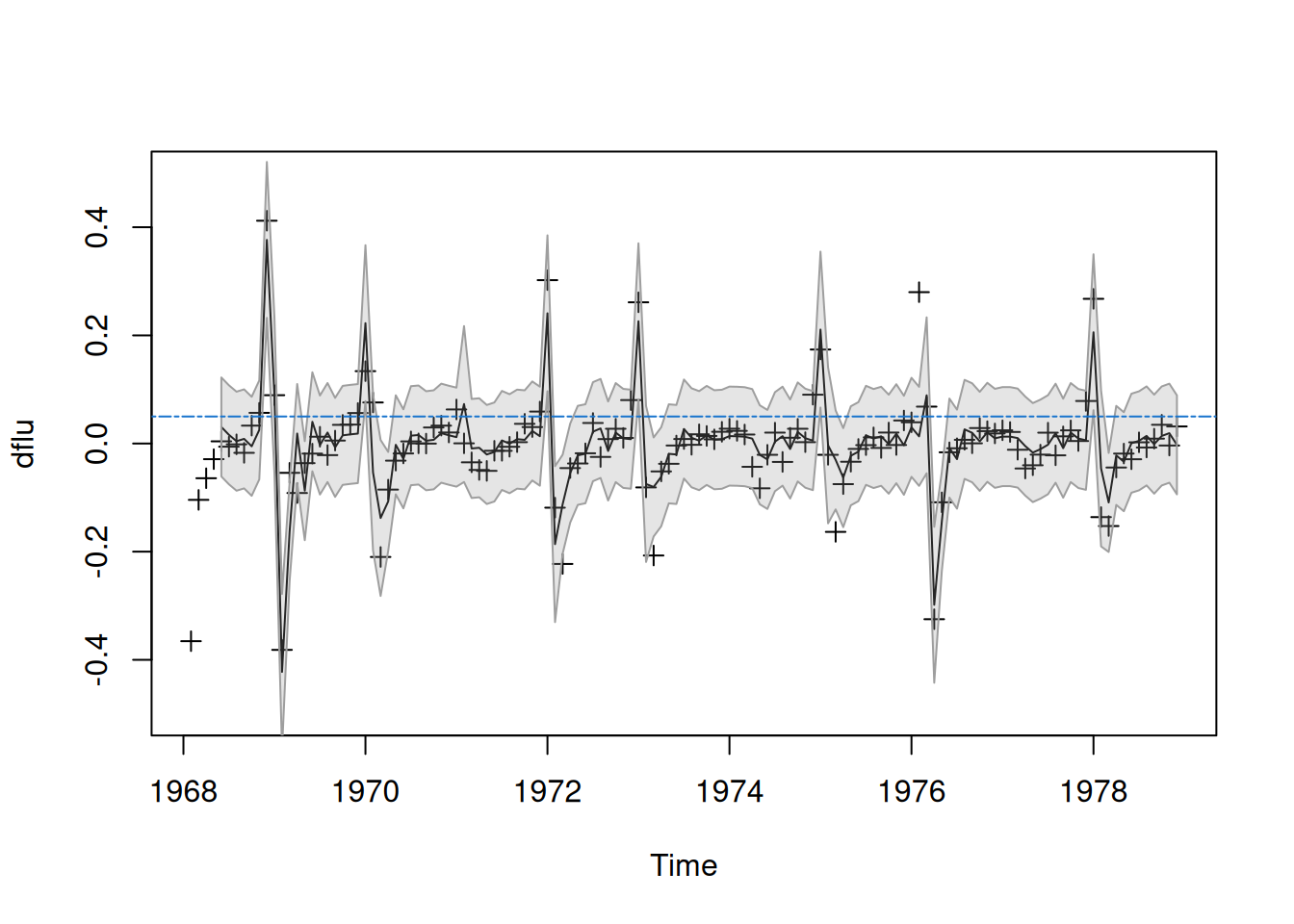

5.3.1.1 Ejemplo: Modelado de la serie de influenza

Se estudia la serie mensual de muertes por neumonía e influenza, \(\mathrm{flu}_t\), que muestra un leve descenso y una clara no linealidad. Para eliminar la tendencia, se trabaja con las primeras diferencias:

\[

x_t = \mathrm{flu}_t - \mathrm{flu}_{t-1}.

\]

Se observa que \(x_t\) aumenta lentamente y luego puede saltar bruscamente cuando supera aproximadamente 0.05, sugiriendo dos regímenes según \(x_{t-1}\).

Errores estándar: \[

\begin{equation*}

\operatorname{se}\left(\hat{\beta}_{i j}\right)=\sqrt{c_{i i} \hat{\sigma}_{j j}},

\end{equation*}

\] donde \(c_{ii}\) es el elemento (i)-ésimo diagonal de \(\left(\sum z_t z_t'\right)^{-1}\) y \(\hat{\sigma}_{jj}\) el (j)-ésimo diagonal de \(\hat{\Sigma}_w\).

Modelo autoregresivo vectorial de primer orden: \[

\begin{equation*}

x_{t}=\alpha+\Phi x_{t-1}+w_{t},

\end{equation*}

\] con \(\mathrm{E}(w_t w_t')=\Sigma_w\)\(k\times k\) y \(\alpha=(I-\Phi)\mu\) si \(\mathrm{E}(x_t)=\mu\).

Identificación con regresión multivariante: \(y_t=x_t\), \(\mathcal{B}=(\alpha,\Phi)\), \(z_t=(1,x_{t-1})\). Estimación condicional de \(\Sigma_w\):

Extensión ARX (exógenas) de orden (p): \[

\begin{equation*}

x_{t}=\Gamma u_{t}+\sum_{j=1}^{p} \Phi_{j} x_{t-j}+w_{t}. \end{equation*}

\]

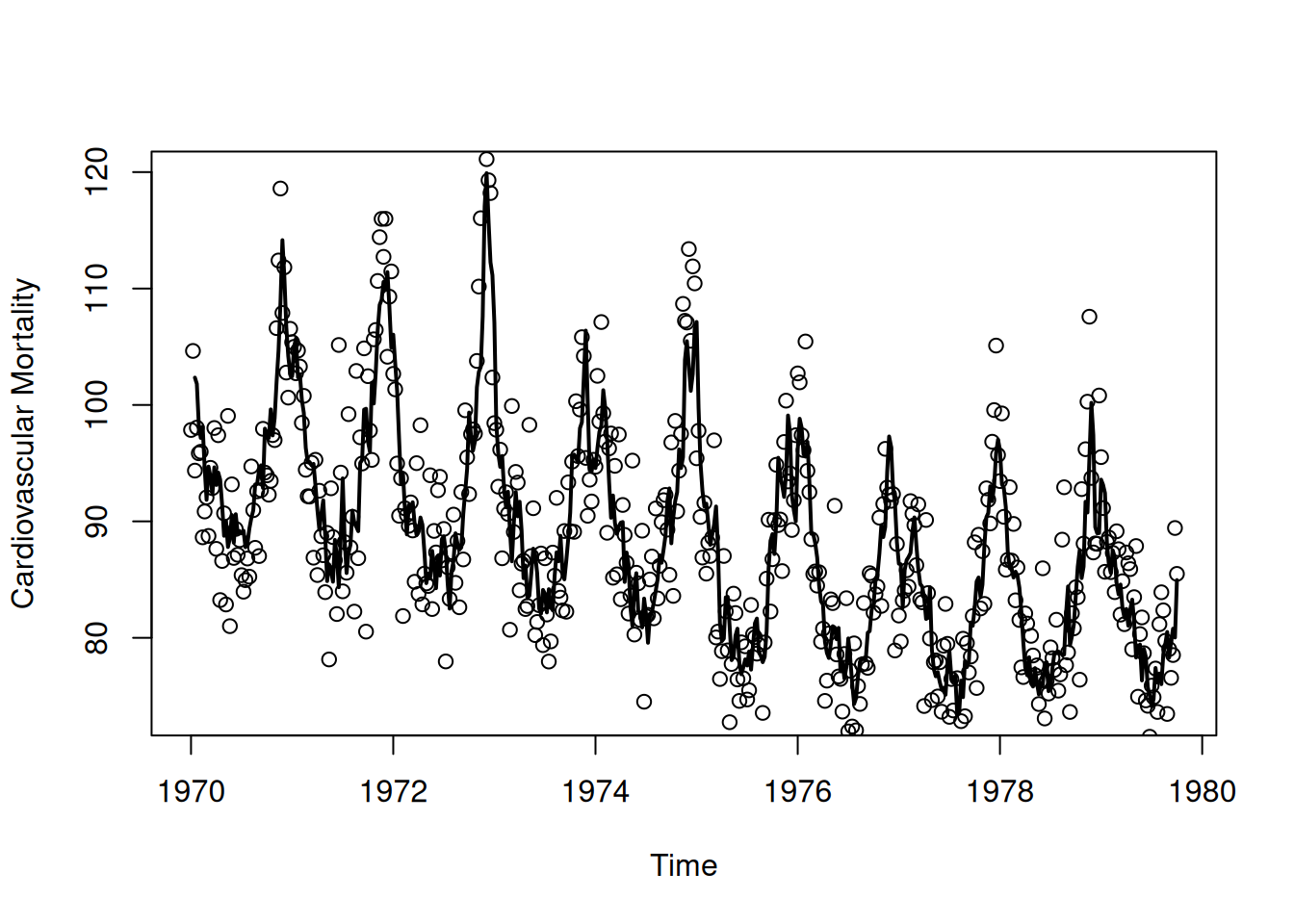

5.4.1.1 Ejemplo (Contaminación, clima y mortalidad)

# Paquete para VARlibrary(vars)

Loading required package: MASS

Attaching package: 'MASS'

The following object is masked from 'package:dplyr':

select

Loading required package: strucchange

Loading required package: sandwich

Attaching package: 'strucchange'

The following object is masked from 'package:stringr':

boundary

Loading required package: urca

Loading required package: lmtest

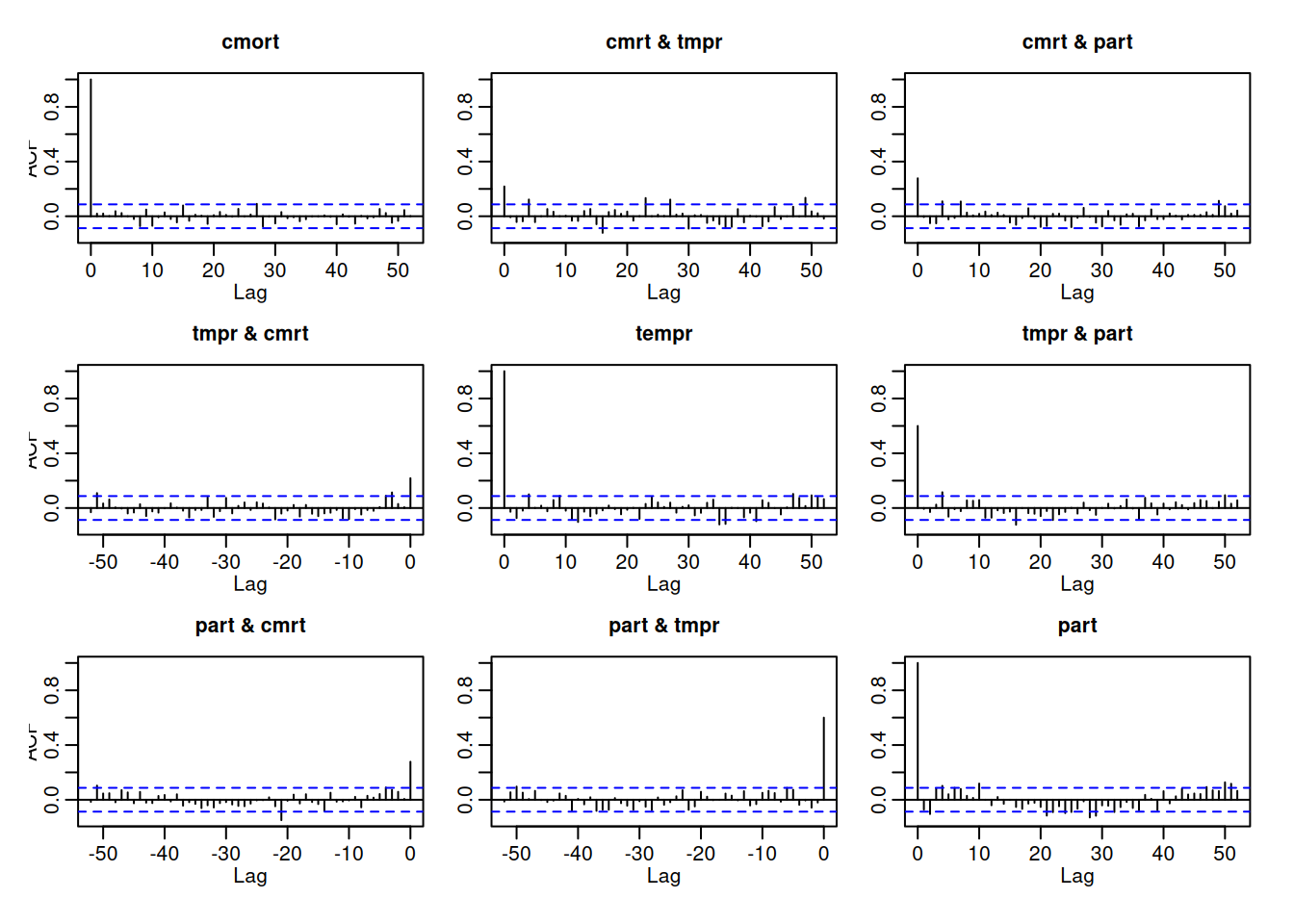

# Matriz de series: mortalidad, temperatura, particuladox <-cbind(cmort, tempr, part)# Ajuste VAR(1) con constante y tendenciasummary(VAR(x, p =1, type ="both"))

VAR Estimation Results:

=========================

Endogenous variables: cmort, tempr, part

Deterministic variables: both

Sample size: 507

Log Likelihood: -5116.02

Roots of the characteristic polynomial:

0.8931 0.4953 0.1444

Call:

VAR(y = x, p = 1, type = "both")

Estimation results for equation cmort:

======================================

cmort = cmort.l1 + tempr.l1 + part.l1 + const + trend

Estimate Std. Error t value Pr(>|t|)

cmort.l1 0.464824 0.036729 12.656 < 2e-16 ***

tempr.l1 -0.360888 0.032188 -11.212 < 2e-16 ***

part.l1 0.099415 0.019178 5.184 3.16e-07 ***

const 73.227292 4.834004 15.148 < 2e-16 ***

trend -0.014459 0.001978 -7.308 1.07e-12 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5.583 on 502 degrees of freedom

Multiple R-Squared: 0.6908, Adjusted R-squared: 0.6883

F-statistic: 280.3 on 4 and 502 DF, p-value: < 2.2e-16

Estimation results for equation tempr:

======================================

tempr = cmort.l1 + tempr.l1 + part.l1 + const + trend

Estimate Std. Error t value Pr(>|t|)

cmort.l1 -0.244046 0.042105 -5.796 1.20e-08 ***

tempr.l1 0.486596 0.036899 13.187 < 2e-16 ***

part.l1 -0.127661 0.021985 -5.807 1.13e-08 ***

const 67.585598 5.541550 12.196 < 2e-16 ***

trend -0.006912 0.002268 -3.048 0.00243 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 6.4 on 502 degrees of freedom

Multiple R-Squared: 0.5007, Adjusted R-squared: 0.4967

F-statistic: 125.9 on 4 and 502 DF, p-value: < 2.2e-16

Estimation results for equation part:

=====================================

part = cmort.l1 + tempr.l1 + part.l1 + const + trend

Estimate Std. Error t value Pr(>|t|)

cmort.l1 -0.124775 0.079013 -1.579 0.115

tempr.l1 -0.476526 0.069245 -6.882 1.77e-11 ***

part.l1 0.581308 0.041257 14.090 < 2e-16 ***

const 67.463501 10.399163 6.487 2.10e-10 ***

trend -0.004650 0.004256 -1.093 0.275

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 12.01 on 502 degrees of freedom

Multiple R-Squared: 0.3732, Adjusted R-squared: 0.3683

F-statistic: 74.74 on 4 and 502 DF, p-value: < 2.2e-16

Covariance matrix of residuals:

cmort tempr part

cmort 31.172 5.975 16.65

tempr 5.975 40.965 42.32

part 16.654 42.323 144.26

Correlation matrix of residuals:

cmort tempr part

cmort 1.0000 0.1672 0.2484

tempr 0.1672 1.0000 0.5506

part 0.2484 0.5506 1.0000

Resultados clave (parciales, en el texto): estimaciones \(\hat{\alpha}, \hat{\beta}, \hat{\Phi}\), \(\hat{\Sigma}_w\) y ecuación de predicción para mortalidad \(\hat{M}_t=73.23-0.014t+0.46M_{t-1}-0.36T_{t-1}+0.10P_{t-1}\) con \(R^2\approx 0.69\).

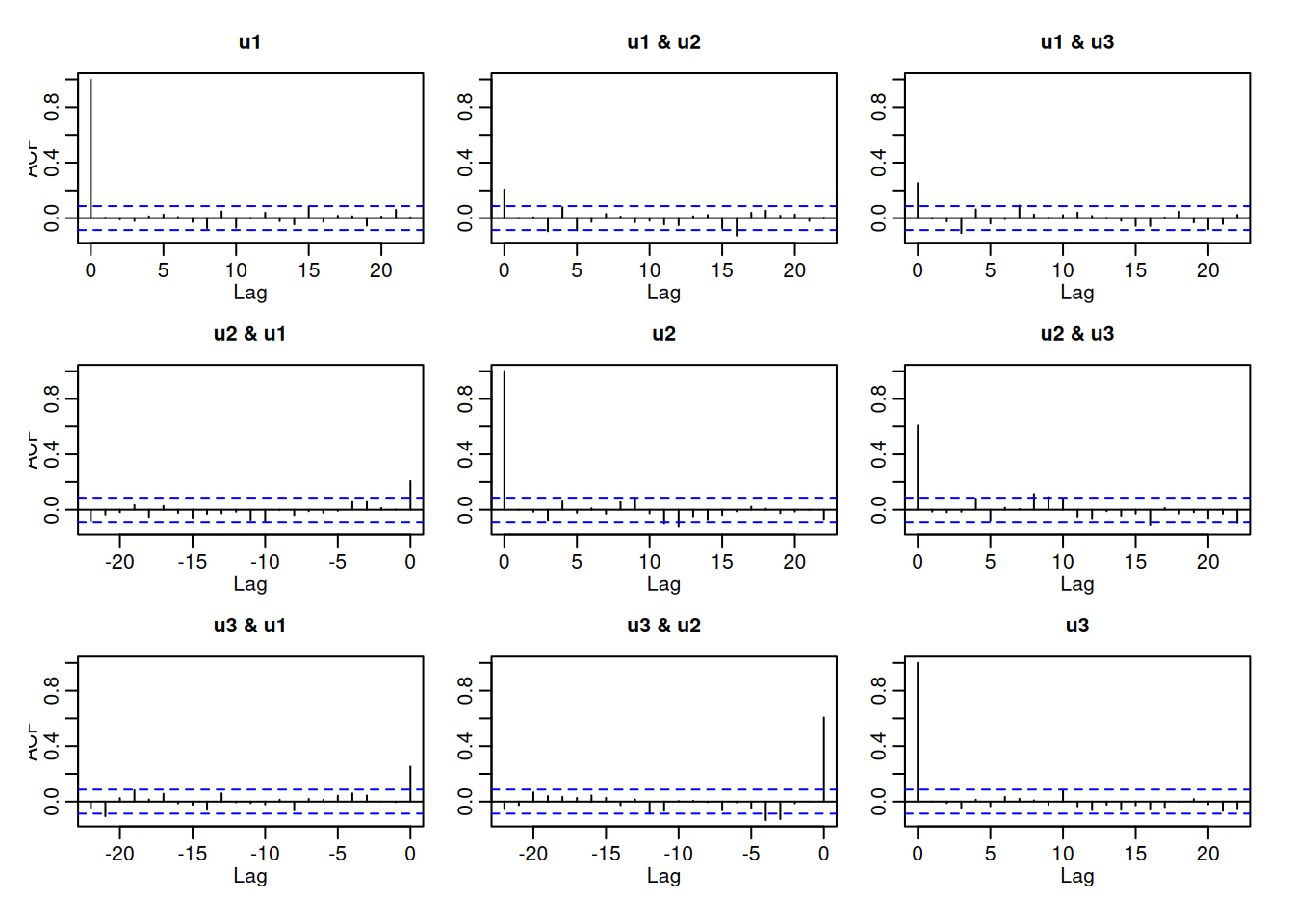

# Diagnóstico: ACFs y prueba Portmanteau ajustadaacf(resid(fit), 52)

serial.test(fit, lags.pt =12, type ="PT.adjusted")

Portmanteau Test (adjusted)

data: Residuals of VAR object fit

Chi-squared = 162.35, df = 90, p-value = 4.602e-06

Interpretación: BIC selecciona (p=2) (frente a AIC/FPE/HQ). El diagnóstico multivariante indica que el modelo no captura efectos concurrentes (correlaciones residuales no nulas), por lo que el test Q (equivalente al Ljung-Box univariado) rechaza ruido blanco.

Sea \(\phi=\operatorname{vec}(\Phi_1,\ldots,\Phi_p)\) (vector \(k^2p\times 1\). Entonces, \[

\begin{equation*}

\sqrt{n}(\hat{\phi}-\phi) \sim A N\left(0, \Sigma_{w} \otimes \Gamma_{pp}^{-1}\right),

\end{equation*}

\] donde \(\Gamma_{pp}={\Gamma(i-j)}_{i,j=1}^p\). Errores estándar a partir de \(\hat{\Sigma}_w) y (\hat{\Gamma}_{pp}\).

5.4.5 VARMA y ARMAX multivariados: operadores y condiciones

Causalidad: raíces de \(|\Phi(z)|\) fuera del círculo unitario; Invertibilidad: raíces de \(|\Theta(z)|\) fuera del círculo unitario. Representaciones: \[

x_t=\Psi(B)w_t,\quad \Psi(B)=\sum_{j=0}^\infty \Psi_j B^j,\ \Psi_0=I;

\]\[

w_t=\Pi(B)x_t,\quad \Pi(B)=\sum_{j=0}^\infty \Pi_j B^j,\ \Pi_0=I.

\]

5.4.6 Estructura de autocovarianza

Para modelo causal ARMA((p,q)) ((h)): \[

\begin{equation*}

\Gamma(h)=\sum_{j=0}^{\infty} \Psi_{j+h} \Sigma_{w} \Psi_{j}^{\prime},

\end{equation*}

\] Para MA((q)): \[

\begin{equation*}

\Gamma(h)=\sum_{j=0}^{q-h} \Theta_{j+h} \Sigma_{w} \Theta_{j}^{\prime}, \quad \Theta_0=I,

\end{equation*}

\] y \(\Gamma(h)=0\) para (h>q).

5.4.7 Algoritmo de Spliid para VARMA (estimación rápida)

Modelo general con media no nula: \[

\begin{equation*}

x_{t}=\alpha+\Phi_{1} x_{t-1}+\cdots+\Phi_{p} x_{t-p}+w_{t}+\Theta_{1} w_{t-1}+\cdots+\Theta_{q} w_{t-q}.

\end{equation*}

\] Si \(\mu=\mathrm{E}x_t\), entonces \(\alpha=(I-\Phi_1-\cdots-\Phi_p)\mu\).

Si \(w_{t-1},\dots,w_{t-q}\) fueran observables, el modelo anterior se puede reescribir como regresión multivariante: \[

\begin{equation*}

x_{t}=\mathcal{B} z_{t}+w_{t},

\end{equation*}

\]\[

\begin{equation*}

z_{t}=\left(1, x_{t-1}^{\prime}, \ldots, x_{t-p}^{\prime}, w_{t-1}^{\prime}, \ldots, w_{t-q}^{\prime}\right)^{\prime},

\end{equation*}

\]\[

\begin{equation*}

\mathcal{B}=\left[\alpha, \Phi_{1}, \ldots, \Phi_{p}, \Theta_{1}, \ldots, \Theta_{q}\right].

\end{equation*}

\]

Actualización de innovaciones (dadas \(\mathcal{B}_0\)):

Los nuevos valores de \(w_t\) se incluyen en las covariables \(z_t\) y se vuelve a estimar \(\mathcal{B}\) hasta convergencia (no necesariamente MLE, pero cercano y útil como inicialización para métodos de espacio de estados).

5.4.7.1 Ejemplo (Algoritmo de Spliid con marima)

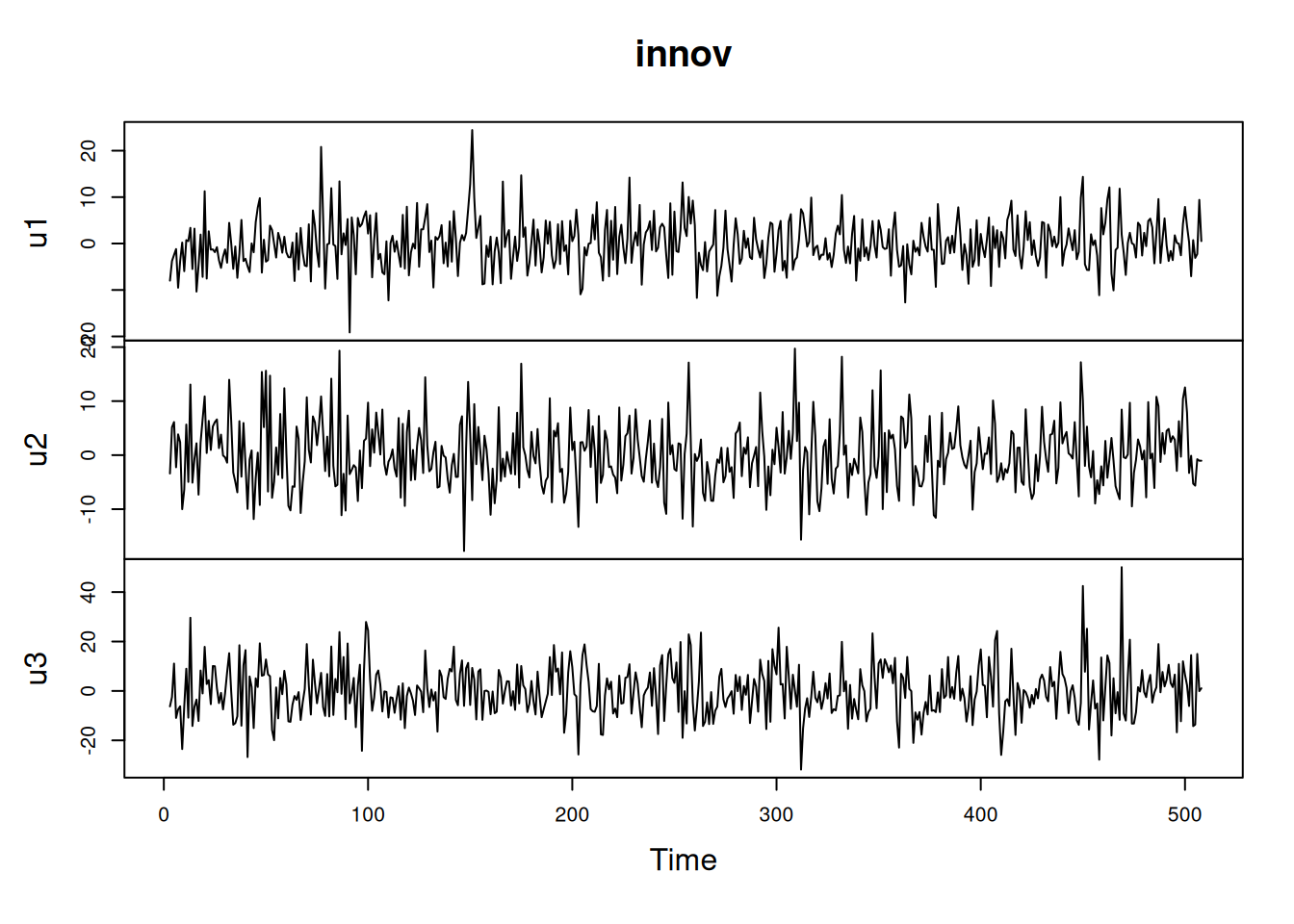

library(marima)# Definición del modelo VARMA(2,1)model <-define.model(kvar =3, ar =c(1, 2), ma =c(1))arp <- model$ar.pattern; map <- model$ma.pattern# Detrendeo de mortalidad (cmort) y armado de matriz de datoscmort.d <-resid(detr <-lm(cmort ~time(cmort), na.action =NULL))xdata <-matrix(cbind(cmort.d, tempr, part), ncol =3) # quitar atributos ts# Ajuste VARMA con penalizaciónfit <-marima(xdata, ar.pattern = arp, ma.pattern = map, means =c(0, 1, 1),penalty =1)

All cases in data, 1 to 508 accepted for completeness.

508 3 = MARIMA - dimension of data

# Innovaciones y diagnóstico (no mostrado)innov <-t(resid(fit)); plot.ts(innov); acf(innov, na.action = na.pass)